I’ve recently decided to start a new series where I interview people who are doing extraordinary things with their lives. First up, I have JP Livingston, who retired at age 28 with a net worth of $2.25 million. And, her net worth is still increasing!

Of that total, 60% of her net worth came from saving, while 40% came from growing her money through investing. This is why investing your money is so important, and it’s how you really allow your money to grow for you!

JP grew up listening to stories about financial insecurity during her parents’ upbringing. The freedom that early retirement brought really appealed to her, and who doesn’t want to retire early anyways?

She is now retired at the young age of 28 and says that she still lives “an incredibly luxurious life.” And, she managed to retire early while living in one of the most expensive places in the world – New York City.

Related articles:

- 21 Best Early Retirement Tips To Help You Retire Early

- Boldin Review: Is This the Best Early Retirement Planning Tool?

- Early Retirement Myths Busted

- Reaching Financial Independence IS Possible And Here’s How You Can Do It

- 75+ Ways To Make Extra Money

- 30+ Ways To Save Money Each Month

- The 6 Steps To Take To Invest Your First Dollar – Yes, It’s Really This Easy!

I asked you, my readers, what questions I should ask JP. And, make sure you’re following me on Facebook so you have the opportunity to submit your own questions for the next interview.

So, below are your questions, along with some of mine.

Here is how JP Livingston retired at the age of 28 with over $2,000,000. You can follow her on her blog The Money Habit as well.

P.S. If you’re curious about what your own retirement could look like, I recommend trying Boldin. It’s a financial planning tool that lets you build your own early retirement roadmap, test out what-if scenarios, and make sure your plan actually works. It’s a great option if you want to retire early—or just want more clarity about your financial future.

1. Tell me your story. How did you manage to retire at 28?

I have wanted to retire since I was about 12 years old. My parents grew up poor. I am talking eight people living in a one room apartment poor. My father’s father passed away when he was 18, and his mother who had previously been a homemaker was only able to find a job at a cookie factory. Her dream for my father was that he would be a busboy and eventually work his way up to be a cook in a restaurant.

My mother’s father passed away when she was in middle school; her mother found work as a seamstress at a large garment factory to support a family of six children.

I grew up on stories of their financial insecurity.

When I started thinking about the future, my parents’ refrain to me was that I could be anything I wanted to be, as long as I had a way to financially support myself.

In middle school, we took a survey on our interests and read about different jobs. I loved to write and wanted to be a writer. When I found out how unsteady the income was for a writer, though, I was demoralized. I decided that if I couldn’t support myself financially by being a writer, I would find a way to retire instead, Then I’d have the freedom work on whatever I wanted, including all the writing I could handle. So I started reading personal finance books.

I learned that you don’t have to be a genius or have special skills to retire early. A habit of making small and regular improvements trumps even the most gifted people who only apply themselves sporadically.

The tactics I’ve employed include optimizing for pay raises and promotions, living a very minimalist and frugal life, focusing on investing skills, and building analytical skills such as understanding how to build and use spreadsheets to support my investment ideas. I found there was an 80-20 rule to different improvements I could make in my money life: 20% of the improvements accounted for 80% of the results. I’ve been trying to outline those major needle movers on my blog so people don’t waste their time as I did on the things that don’t really matter.

All those incremental improvements stacked up into a humming, healthy machine. When I retired at 28, I had a net worth of $2.25 million and it’s still climbing.

2. How did you reach $2,250,000 in savings by the time you were 28? When did you begin saving?

60% of my net worth came from saving and 40% came from growing my money through investing.

My saving habits started in childhood, which isn’t surprising given my parents’ experiences. But what really upped my game was branching out from a few good habits and awareness to trying to find unorthodox ways to save.

One savings move that went against the grain was graduating college in three years. I earned scholarships to attend a state school for free but I chose a private college which I felt would offer broader opportunities. That private college was incredibly expensive though. So in compromise, I graduated a year early.

The savings from that move was not just the tuition costs, but also a full year of missed earning opportunity. My first job was in finance and paid $60,000, with a promise that that if you stuck it out through the entire year you got a bonus that was almost equal to your base. So that one decision to graduate early caused a nearly $150,000 net worth swing.

That kind of savings so early in life, growing at market rates for 20 years would yield $800,000 by the time a person were 42. That’s enough for some people to retire through one decision alone!

Related: How I Paid Off $40,000 in Student Loans in 7 Months

3. What made you want to retire early?

The freedom is really what appealed to me.

I had a very potent reminder of how important freedom was and how little time I had to enjoy it the year before I retired. There were several deaths and major health scares amongst my loved ones. That made me realize that given my family’s history, I had about 15 to 20 really good years of health that I could count on. Did I want to spend even one more of those years stressed out while working?

4. What sacrifices did you have to make in order to reach this milestone?

I’ve rarely thought of my financial decisions as sacrifices. Rather, they were decisions to purchase one thing over another. If I took my bonus into the store and were deciding between a cool new phone or a camera, I wouldn’t leave feeling like I had “sacrificed” the one I didn’t purchase.

I wanted to buy back my time and my freedom more than I wanted to buy anything else in the store. In short, I’ve looked at this is as an opportunity, not a sacrifice. That does wonders for your motivation and mental health.

There is an excellent book that I think provides one of the best frameworks to thinking this way. It’s called Your Money or Your Life, written by Vicki Robin and Joe Dominguez. The general concept is this: take the amount of money you make in a year. Subtract out all your work-related expenses. Now take that balance and divide it by the number of hours you work. That gives you the amount of money you are exchanging per hour of your life. With that metric, you could estimate how many hours of your life a purchase would cost rather than dollars.

Once you start looking at your purchases this way, you will want to buy much less. And investing will start to look amazing to you! It’s a magical way to get more of your life back, because those dollars can go to work in your place, earning you money while you sleep.

5. Would you say that you live comfortably?

I think we live an incredibly luxurious life. There’s still a ton of fat we could cut.

6. What career did you have before you retired? Did that career help you to retire earlier?

I was a professional investor at a finance firm and it definitely helped me to retire earlier. I got really lucky that it ended up being so lucrative; I initially planned on it being a two year stint at most. But the work kept getting more interesting and the pay got better. The frameworks we used for investments also helped me think about my own investment decisions for my personal portfolio.

7. What do you have to say to those who may think that they can never earn as much as you can – can they still retire early too?

They can absolutely retire early!

To me this is the whole point of why the personal finance blogosphere exists. None of us have identical circumstances and identical outcomes. Your childhood may have been more or less advantaged than mine. Your lucky breaks might be better or worse than the ones I experienced. But the absolute truth is this: the you that is making consistent, small improvements over time to your money plan is going to easily accumulate 5x the wealth of the you that isn’t.

It’s not hard to retire early in this country because the bar is so low. The average age of retirement in the US is age 63. After 41 years in the workforce the average 63-year-old couple has a total net worth of $174,000 to show for it. That works out to just over $4,000 of savings per year; less if you assume any investment growth.

8. What do you do now that you’re retired?

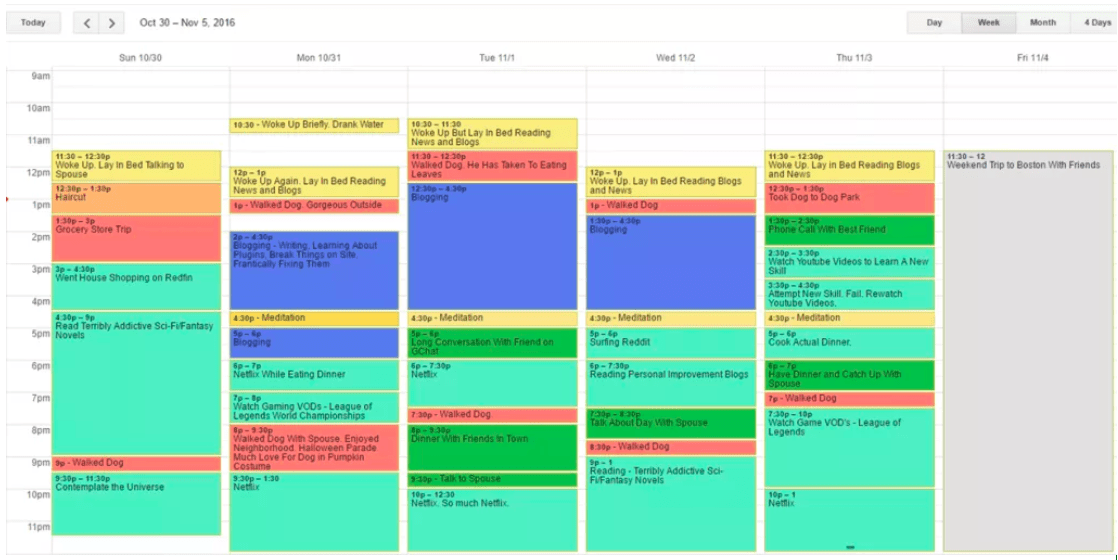

The best thing I can do is show you. Here was my actual calendar from a recent week:

Broadly speaking, I have one major project – a personal finance site I write to help others retire early – which I work on for about 10 hours a week, then the rest of the time is filled with hobbies, reading, and being out in the city.

It is amazing how enjoyable the mundane things are when you are not too stressed out to notice them.

9. Many people will have this question in the comments of this interview, I just know it! – Can you explain how you will make $2,250,000 last your whole life, even though you are only 28?

That’s a great question.

My plan is based on data gathered by the Trinity Study. This study calculated that if deployed in a portfolio of stocks and bonds, an inflation-adjusted 4% yearly withdrawal rate from savings was optimal to safely retire and not work for a given 30-year window in the history of the United States.

Thus, if your annual expenses is equal to that 4% yearly withdrawal rate, the idea is that it is very unlikely you will run out of money in a 30-year period.

However, I have some concerns about the riskiness of that 4% figure. For one thing, my retirement is expected to be much longer than 30 years. In addition, if you look at stock market performance in the last 20 years, the compound annual growth rate was 8.2%, almost 2 points lower than the CAGR shown in the period the Trinity Study originally measured. For these two reasons, I plan to live off a stock and bond portfolio withdrawing an inflation-adjusted 3%.

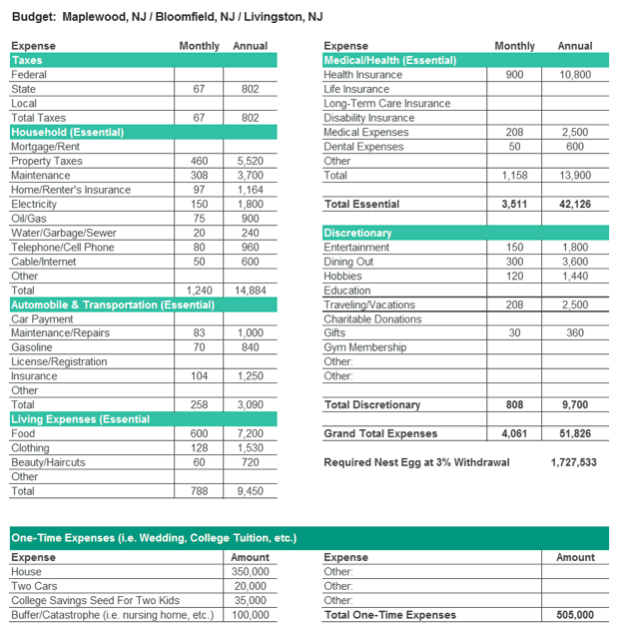

3% of my $2,250,000 would give me $67,500 a year. My husband and I currently spend $65,000 a year living in one of the most expensive cities in the world. That means we could support our current lifestyle almost indefinitely.

But one of the hard parts about retiring so early is that you have to plan for chapters of life that could look drastically different than today. Having children, for example. So before I pulled the trigger, I built a projected budget for a family of 4 to calculate how much I would need to support a family. I did this with empirical data, researching what actual families of four paid for the service in the city I was considering.

The nest egg required to support this budget is $2.23 million, which is within our means.

With early retirement specifically, I think it’s also comforting to walk through your other margins of safety that don’t show up in the budgeting process. Here are a few in our case:

- Conservative Withdrawal Rate: We are using a withdrawal rate some would argue is half to one percentage point more conservative than needed. That would equate to overstating my nest egg needs by over $400,000.

- Extra Buffer: We have an extra one hundred thousand dollar buffer that will grow over time and which will absorb costs we haven’t foreseen (i.e. higher healthcare premiums, poor market performance for a year, etc.).

- Full-Time Work: Either of us could go back to work full time.

- Income-Earning Hobbies: One or both of us might end up doing a hobby that generates money

- Tighten Discretionary Purchases: $9,700 or 19% of our annual budget is discretionary and we could tighten our belts in a particularly rough year just as every other family does.

- ACA Healthcare Savings: We have not factored in any ACA subsidies even though our income in this budget would qualify us.

- Market Outperformance: Markets could do better than we’ve projected. We require a blended 5-6% return (3% withdrawal, 2-3% inflation). We could easily see market CAGR of 8%+ as evidenced by historical data.

- Home Equity Loans/Reverse Mortgage: We can draw cash out through a home equity loan if we have a temporary cash crunch or use a reverse mortgage in our old age.

- Profit-Share Grants: My profit-share grants from my previous employer may be worth greater than the $0 we’ve estimated.

10. Do you still earn an income?

Not currently.

I am not ruling out a traditional job one day, but it would be about finding interesting work and less about the money. My goal right now is to create a place that helps other folks get smarter about money and retire faster, so I might do some freelance writing outside of the blog. But I don’t want to have left one job just to jump into another!

As for other forms of income: I do have some deferred compensation from my old employer. And although my husband could retire as well, he likes what he is doing and continues to work.

11. How did you decide on how much you needed to retire on?

I was a professional investor and the way we used to make our investment decisions was to build out various scenarios, observe the outcomes, and attach a probability to each. I did a similar exercise for determining how much I needed to retire. I used three scenarios to triangulate on a target number. There’s a walk through on the three scenarios which anyone can use to determine their own target retirement number over here.

12. If you were starting back at ground zero, what would you do differently from the beginning?

Two things:

- Put Momentum First: I would focus on building momentum more than trying to muscle my way through things with sheer discipline. Most people’s initial reaction to starting a new project is to throw themselves all in. I get emails asking me what book I’d recommend people buy to turn their financial lives around. But think about how you got into your other hobbies. Did you run out and buy a book about proper free-throw technique to get into basketball? Were you consulting a textbook to get into yoga? If the key to millions of dollars is showing up every day and making small improvements, then the key to your success is figuring out how to build momentum in those early days that will get you showing up regularly. That means less of a focus on running out and buying dry, boring textbooks and more effort on joining blogs or forums with bite-sized, regular content where you can start to get your bearings and get interested.

- Tackle The Right Steps In The Right Order: There are four steps to early retirement, and tackling them in the right order really accelerates your progress. I wish I had thought deliberately about how the levers in front of me were changing and better prepared myself for the different stages. I’ve missed a lot of great opportunities because I was so focused on the things that had been working for me in the past that I didn’t look up and think about the new opportunities open to me as my wealth accumulated. For example, I wish I had understood the math behind investing in high-appreciation real estate markets year ago. If I had, I would have bought a house in NYC years ago and be $500k richer.

13. Is retiring everything you thought it would be or not as you planned? Do you ever miss work?

It is a hundred times better than I thought it would be. I will admit there was a learning curve at first. But these days, I often tell my family that I am living a version of my dream life. If you had known me before I retired, you would have found that statement astonishing.

If there is one thing I miss about work, it’s regular interaction with smart and thoughtful people. Since I started the blog, though, I’ve gotten quite a bit of that back. So overall I’m quite happy!

14. Lastly, what is your very best tip (or two) that you have for someone who wants to reach the same success as you?

Ask questions. Be the active commenter on a blog or the vocal one at the cocktail party. Be courageous enough to cold-email the people you know have the answers you need. You can learn so quickly if you’re willing to put yourself out there. People are generous with their experience if you show you’ve done your homework and ask them specific things that make it easy for them to help you.

“Why?” is your most powerful tool. If someone tells you investing in X is the way to go, ask why, and pepper them with all the potential concerns you can think of. Then go find another smart person and ask them why X is a good or a bad idea. Go back to the first and pose the second person’s counterargument and ask them to respond. Introduce another expert. Repeat until you feel you understand the issue backwards and forwards. This is hands down the best way I’ve found to master a concept.

Focus on habits and systems, not results. You can make yourself feel really good by muscling through a one week sprint with discipline and admiring what you accomplish. But really impressive results take weeks and years of focused effort. I have seen a lot of amazing people in college and at my old employer, and the thing that separates the average from the incredibly successful is really just who has figured out how to put out consistent effort. No one has discipline to last in a marathon like this without building the right systems and habits. Show up every day and do one small thing to improve the thing you’re measuring. If you do this, you will be among the top 5% of achievers. Over time you will build a system that will trump any specific lucky breaks or windfalls, and it will get you to financial success you deserve.

Are you interested in retiring early? Why or why not?

Leave a Reply