Today, I have an article from Penny. Her family of six spends just $53,000 a year, with $22,000 of that going towards their student loan debt. Here is her story.

Today, I have an article from Penny. Her family of six spends just $53,000 a year, with $22,000 of that going towards their student loan debt. Here is her story.

Dear Readers of Making Sense of Cents,

I’m Penny. I write a blog with my cousin, Rich. It’s called Penny and Rich. He’s rich. I’m poor. Get it? I’m a stay-at-home-mom with four kids. We have a household income of $43,000 a year and my husband and I have over $153,000 in student loan debt. Rich is a busy professional with a household income of $250,000 and he is well on his way to becoming a millionaire. This blog is our way of writing to and trying to understand each other, financially and otherwise.

We accumulated this massive student loan debt when my husband went back to school to become a chiropractor. He has been in practice almost six years now.

It’s doing better every year, but it’s taken a lot longer to grow a business than either of us thought it would.

We don’t regret taking out the loans, because we value having me staying home with the kids and family time over money and debt and everything. And, honestly, having the debt is not that big of a deal.

Rich doesn’t understand how my family of six can get by on such a small income, let alone tackle our massive student loan debt. But let me tell you, dear readers, how we are going to do it. Maybe you can make sense (that’s a shout-out to you, Michelle!) of our madness.

Related:

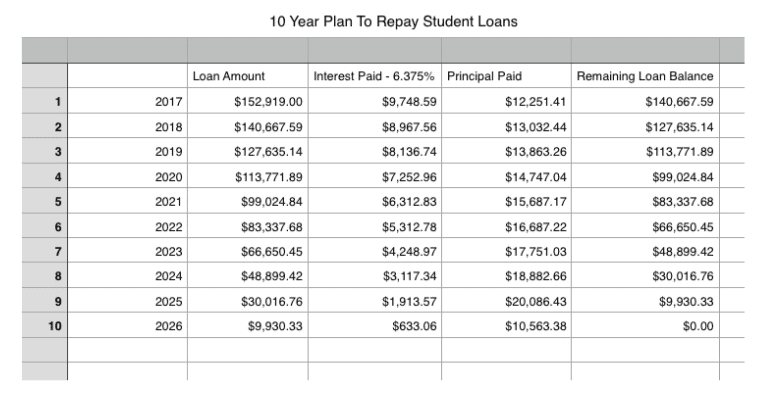

Our 10 Year Plan To Repay $153,000 in Student Loan Debt

Very simply, we are going to put $22,000 toward the debt every year. Here is a spreadsheet of what that is going to look like:

(Keep in mind that this spreadsheet is an estimate, because student loan interest is typically compounded daily, and I didn’t want to work through those sorts of calculations when creating the spreadsheet.)

$1,000 is taken out of our checking account automatically every month (for a total of $12,000 a year), plus an additional $10,000 will be thrown at it when we get our tax refund. This will eventually make a dent in that massive behemoth of a loan, and we will have it paid off entirely in 10 years.

Right now, it feels like we’re doing nothing more than throwing money at a wall. So much of it is going toward the interest. We have to pay $812 a month just to keep the loan from getting any bigger. Which sucks. At the end of the 10 years, we will have paid over $55,000 on the interest alone.

We’ve tried to refinance the loans, which is where all the really cool, fiscally responsible people are going, but they won’t have us given our debt to income ration (which, of course, makes sense on their end)…

But here’s another thing:

We are on a Income-Driven Repayment Plan with our lenders. This means that we make payments in accordance with our income. Right now, they are requiring us to pay:

$0

And they will forgive any loan balance remaining after 25 years.

Sounds like a pretty sweet deal, right?

So, why are we putting $22,000 a year toward student loans when we technically don’t have to pay anything and the remaining balance will be forgiven anyway?

Well, let me tell you, because here’s the catch: We would have to pay taxes on the amount forgiven!

So, let’s say we continue to remain at this income level ($43,000), or thereabouts, for the next 25 years, and let’s say we pay $0 the whole time. At the end of 25 years, due to the constant growth of that friggin’ interest, the loan will have amassed itself to an astounding:

$716,865

Thanks to this little handy Tax Calculator, I can calculate that we would have to pay $229,545 in taxes on that amount, which is actually $9,545 more than what we would pay doing my little 10 Year Repayment Plan thingy.

(Plus, we’re the ones who took out the loans, we’re responsible for paying them, and we really do want to be able to pay them back. Blah, blah, blah.)

So, now, a question you’re probably asking yourself is:

How in the world can you afford to put $22,000 toward student loans when you have an income of only $43,000 a year (and four kids to boot)?

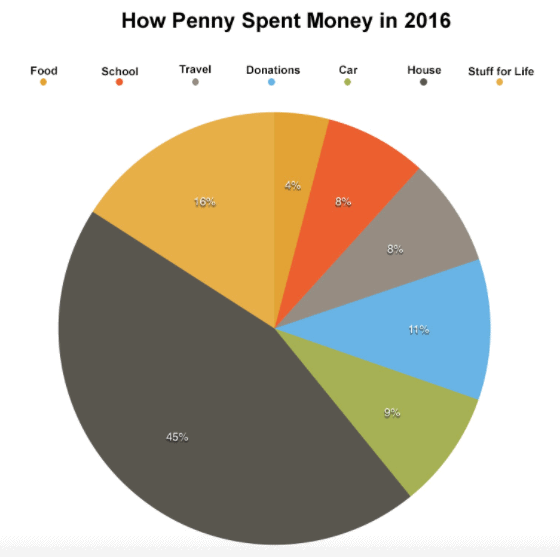

First, let’s take a look at how we spent our money in 2016, and we’ll get into it:

Okay, so now you’re going to have some more questions here. And your first question is going to be:

How did you spend only $528 in food to feed your family of six?

Well, dear readers, here’s our deep, dark secret… since we are low income, we get the majority of our food covered by Food Support. I’ll write more about that at the end of this post, but, for now, there you have it. We get Food Support, and this enables us to put more of our money toward student loan loan debt.

Which will bring you to your next question:

Where are those student loan payments anyway?

For some reason, I like to keep them separate in my head (and therefore in this post). Since we are not *technically* required to pay them, I see it as a *somewhat* nonessential expense (although, really, it isn’t, I know this).

So, with the loan payments, our grand total of expenditures in 2016 was actually:

$31,942.03 in regular expenses

+$22,000.00 in student loans payments

$53,942.03 total

Which brings us to your next question:

But Penny, you’re only making $43,000 a year? How can you pay all that?

My second deep dark secret, dear readers, is… we get a massive tax refund every year.

Let’s look at these numbers:

$7,321 – 2015 Federal Tax Refund

$2,655 – 2015 State Tax Refund

$2,006 – 2015 Property Tax Refund

$11,982 – Total

So, add that number to the $43,000 in income that we made, and we get:

$54,982.00

There, now we’re ahead of the game.

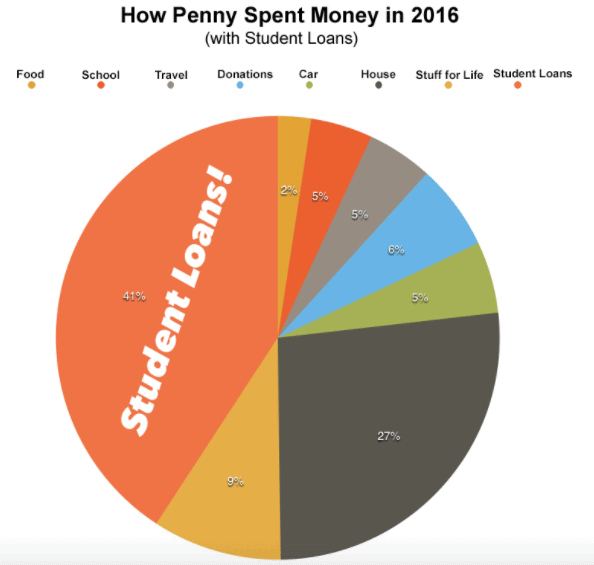

Let’s put together some fun charts on this. Here’s a look at what we spent our money on in 2016:

Okay, and now let’s see what it looks like with the student loan amount thrown in:

Pretty crazy, huh? Good thing I have that 10 year plan!

Now, about Food Support…

As I mentioned earlier, our family gets food support. We’ve been getting it for about eight years now, ever since my husband started chiropractic school. We could have gotten it before then, when he was a Catholic elementary teacher making only $18,750 a year, but I hadn’t known it was available to us. I didn’t realize we were poor.

When we first started getting food support, I wasn’t sure how to feel about it. I was kind of embarrassed. I felt like we were too good for it, like we were above it.

Now, I receive it with gratitude. I know that we are not any better or worse than anybody else getting it. I am no longer too proud.

Could we get by without it? Yes.

Do we use what we save on food to help pay off our student loan debt? Absolutely.

Is that fair? I think so.

I recently read this amazing book called The Art of Asking by Amanda Palmer. In the book, she writes this little tidbit about how Henry David Thoreau’s mother would bring him donuts while he was squirreled away working on Walden:

The idea of Thoreau gazing thoughtfully over the expanse of transcendental Walden Pond, a bluebird alighting onto his threadbare shoe, all the while eating donuts that his mom brought him just doesn’t jibe with most people’s picture of him as a self-reliant, noble, marrow-sucking back-to-the-woods folk hero.

I think a lot of the time, people might expect those getting government assistance to look and act a certain way (poor), and that they shouldn’t be able to enjoy any kind of treat or luxury (like going to Harry Potter World) because of that. Kind of like how we expected Thoreau to look when he was living at Walden Pond.

It’s not the act of taking that’s so difficult, it’s more the fear of what other people are going to think when they see us slaving away at our manuscript about the pure transcendence of nature and the importance of self-reliance and simplicity. While munching on someone else’s donut.

I’m not working on writing a literary masterpiece here, of course. I’m just trying to raise my kids while my husband tries to grow his business… and, yes, all while we’re munching on someone else’s donut.

And I’m okay with that. I’m learning how to take the donuts.

It is a gift to be able to accept support from another person (or the government). It makes you humble. It makes you grateful. It makes you human. It is a gift to be able to give, and it is a gift to be able to receive.

Unlike before, I am slowly starting to realize that I am (kind of) a poor person. However, I still don’t feel like one (I think being “poor” has less to with money than one might expect). In many ways, I live a life similar to wealthy people, just one with a lot more support: We send our kids to a private school (thanks to a scholarship), we eat healthy, organic food (thanks to food support), and we own our own home (thanks to our moms co-signing on the mortgage).

Should my life look differently? Should I look like I am poor and suffering? Or should I gratefully take the donuts and do what I can with them?

That’s the road I’m taking.

And is that fair? A lot of people, like my cousin Rich, have worked hard to get where they are and for what they have acquired. But have they worked any harder than my husband worked in chiropractic school and in starting his own practice? Probably not. Do busy professionals work any harder than construction workers or a teachers do?

It’s all relative. Different people have different interests and values and jobs and income levels. And some people just get lucky. (Even Rich recognizes that we all have a role to play, and he wrote a parable about how we are different types of squirrels and our conversations make the “forest” a better place.)

We all need to take care of each other, in any way that we can. We belong to each other.

And that’s a good thing.

Here’s another excerpt from The Art of Asking (I can’t recommend this book enough) that sums this up:

Our first job in life is to recognize the gifts we’ve already got, take the donuts that show up while we cultivate and use those gifts, and then turn around and share those gifts – sometimes in the form of money, sometimes time, sometimes love – back into the puzzle of the world.

Our second job is to accept where we are in the puzzle at each moment. That can be harder.

I recognize that our circumstances are unique. There probably aren’t a lot of people making $43,000 and putting $22,000 toward student loans every year. I hope to be at the another place in the puzzle in the future, a place where I can share more of my gifts and take less. Until then, I think it’s good to have conversations like this… conversations about money, about life, and about our place in it all.

Low-income people are not usually represented on personal financial blogs. I want my cousin, Rich, to understand what it’s like, and I want you, dear readers, to understand as well.

And along the way, we all might learn something from each other.

Thanks for reading,

Penny

Do you have any questions for Penny? What are you doing to pay off your debt?

Leave a Reply

Really excellent report! My only suggestion is this (and I appreciate that you want to pay your loans but in the interest of fullness): You’ll surely have to pay taxes on your forgiven loans. That said, the tax due could be lower than you return if you were investing the money elsewhere and could draw a higher rate of return. This is super risky and has no guarantee of return, but if you could make more than the 10K than it’s worth a look.

One question: are there loan forgiveness programs for health care professionals that do public service? Maybe your husband can look into a community health program where he could volunteer some services.

And to the commenter that asked what Food Support is: SNAP, Benefits, Welfare, Food Stamps etc. Yes all programs to help people get appropriate nutrition.

I’m not sure about loan forgiveness programs for health care professionals that do public service. I don’t think so, if I’m remembering correctly from when I looked into it. Thanks for the idea though. And the investment idea… it’s a good one, just a little too risky for my taste. Plus, I don’t think I’m knowledgeable enough in that arena to do any good.

Oh man, these folks with their “if you can afford to take vacations, you can afford to pay for your own food.”

Sorry, but I am quite content with my tax dollars paying for the food of folks like Penny and her family. I have to wonder what sort of experiences the commenter has or hasn’t gone through that has left her with such a lack of empathy.

Anyways, Penny, thank you so much for sharing this. I thoroughly enjoyed reading it. I feel like so much of this personal finance space is filled with single people or people with no kids trying and succeeding to get rich. I haven’t ever seen a family like yours share their “behind the scenes” details on how they make it work, i.e. the experiences of making difficult decisions. I will be checking out your blog. Thank you for your honesty!

Hear, hear, Whitney! I totally agree. So much of our tax dollars are wasted on nonsense, I’m happy to know the loads of taxes my husband and I pay as a married-without-kids family go to people to help them eat.

I liked Penny’s post too because it was helpful for me to see how she budgeted! We’re almost in the same boat as she is except for a few differences, and I was always wondering how to find more money to throw at my loans. To the point, I like how she laid out her PLAN – I could find more money, I’m sure, but such large debt #’s make me think it’s impossible. Penny shows it’s NOT impossible!

Thanks, Melissa.

Thanks, Whitney.

Hi Whitney — I’m Rich, Penny’s cousin and the other half of our blog.I think there’s a lot of ink and vitriol being spilled these days over rich people (selfish!) and poor people (lazy!), and the thing is, you don’t really know how someone got to their situation without listening to them first, and having a conversation. So thanks for listening!

Hear hear!

Great job paying down that debt while providing for your family! We’re married with no kids right now, so we have the chance to really pay these suckers down. Everyone’s situation is different, but what matters is that you’re able to pay them off in the best way you can.

Yes, and I think it’s a great idea to get as much of your debt paid down before having kids, so good job there.

I appreciate your openness and hope that things work to plan.

10 years is a very long time to live so close to the edge. Obviously, the self-employed income should go up over time. But unless I missed it you are not saving for retirement, don’t have life insurance or long term disability.

So if something happened to your husband and he wasn’t able to work or he passed away you would be in a very bad position.

It sounds like you may want to re-evaluate his work choice by joining a more established chiropractic office, moving or getting a part time job to attack more of that debt. He doesn’t really have the luxury of not maximizing the earning potential of his degree with that much debt.

What you have going works if it works but doesn’t leave a large margin for error beyond the general social safety nets.

I hear what you have to say, and you remind me of my cousin who writes on the other half of our blog. The thing is, we don’t feel close to the edge. We live simply and feel that we have everything we need. We’re happy and content and doing fine with our lives. My husband and I don’t want to compromise on the chiropractic office he is choosing to operate, or the family time we are choosing to have in order to maximize our earning potential. That is not what life is about for us, and we are better than okay with that.

But, yes, I do agree with your last sentence especially, but we are okay with that (what I view as a minimal) risk.

Hey M Bowden — I’m Rich, Penny’s cousin and the other half of our blog. This is actually my biggest point of disagreement with Penny and I’ve learned I can’t convince her. We are both stubborn! (must be related)

Bad breaks (car accidents, etc) happen all the time to very good people, and a little life insurance can be the equivalent of a financial and societal seat belt. Interesting that we are required to have car insurance but not required to have life insurance.

I actually wouldn’t even quibble with Penny not feeling “on the edge” right now. The reality is that even my family, with a $250k annual income, would be scrambling if tragedy struck. Everyone is one or two bad days from being on the edge, right? So, in my view, life insurance is a good idea for everyone. Cheers! –Rich

My husband has a mental illness diagnosis so life insurance is incredibly high. However, when I crunched the numbers I found that social security survivors benefits for our kids almost replaces his income. I’ll bet that with their income being on the low end that’s probably the case for them as well. That money would give her time to transition to earning an income of her own if he were to pass away.

I’m sorry, but if you can afford to take vacations, you can afford to pay for your own food.

Define “afford vacation” – there are many different kinds of vacation spending — some are extravagance and some are low budget, and some are even free – now a days, many are having staycations. Europeans takes a lot of vacations and it’s no wonder they’re healthier than most hard-working Americans struggling to get by and end up paying for counseling from stress. Stress is the #1 killer in our world. Vacation is to replenish the body, the spirit, the minds and bonding for families. Once the kids grow up, that’s it.

I am not impressed at all with you taking food stamps (paid for by our tax money) with an income of $43000. That is one of the reasons our economy is such a mess. Going out to eat,taking vacations and I believe you used the word luxury. Sorry this is totally wrong. Not sure how you can sleep at night.

Hi Melanie and Carolyn — I’m Rich, Penny’s cousin and the other half of our blog. I admit, these thoughts crossed my mind as well. They cross everyone’s mind, so I don’t blame you for saying it. I’m not sure what I’d do in Penny’s situation, but we’re different people and I’m an ambitious guy, so maybe I’d be working 3 jobs and missing my family in the process. Maybe that would lead to greater stress and to divorce and child support and so on. If there’s one thing I know about Penny, it’s that her family is strong and her kids will be in a good position to contribute to society. That is a social good that lasts generations.

What I’ve learned from Penny is that low income people are human, and every choice isn’t a choice about money even if I might do things differently.

Either way, I appreciate your honest reaction. –Rich

Both spouses working does not threaten divorce. The relationship should be built with stronger substance than that. I grew up with a single mom who worked 3 jobs while my brother and I stayed with aunts or grandparents when she was at work. The funny thing was, I don’t remember that being a bad experience. We were always poor but as a child, I didn’t feel it. My husband and I eloped, rented a room for the first year of marriage before we could qualify for an apt and even then had to get a co-signer. We lived in a 1 bedroom apt with 2 of our kids for 4 years while he finished school. Again I say, it’s a matter of choice. I was low income for 12 yrs of my marriage, and now we are in a good place because we both worked at making it happen. Me working or owning a business also opened opportunities for my husband to find jobs as well as him working and owning a business opened opportunities for my kids and I.

Yes Carolyn, bc low income people don’t deserve nice things. How do you sleep at night being such a hateful twat? Anyway. You do realize that you pay under $10 A YEAR towards SNAP, right? If you’re of average income, it’s more like $3. And that is towards the entire nutritional program, NOT just SNAP benefits. If you’re going to get so pissy over contributing what amounts to less than a value meal, maybe you should move back underground with the rest of the trolls.

Agreed. Our family has taken two vacations- driving to visit relatives for family events- in 20 years. Ideal? Not in the least, but it’s all about priorities. We are not on food stamps or public assistance- I was taught to pay my own way unless it is *truly* impossible, and to accept financial help for life-sustaining needs only, for as brief a time as possible. Choosing to be self-employed, paying down loans at higher rate than may be feasible, and yes, vacations, are all priorities of luxury when you’re accepting money from your neighbor’s pocket. We scrimp and go without so we don’t have to, and frankly, are disappointed when others take advantage of a system meant to help those fallen on hard times until they work their way out as quickly as possible.

I realize this will be an unpopular opinion, but it’s honest, and has evolved through lots of self-examination, observation, and trials over the years. People need to really grasp that the government has no money of their own to give you- that public assistance is dipping into your friends’ and neighbors’ pockets so you can obtain something they may not even have themselves, and that many of those friends and neighbors are running out of money.

It’s utterly amazing to me that many people have no idea that the government has no money of its own. It only has the dollars that it takes from those who have earned it to distribute as it sees fit. So when someone tells me it’s government money, I realize it’s a losing battle.

I’m more in your boat too. While my husband was attending professional school (meaning he did not have a job because of the strenuous workload required by his program), I worked the night shift at the hospital so that we could stay afloat. I was exhausted during the day taking care of our boys (childcare is expensive) and we didn’t get to take vacation: all spring and Christmas break I was picking up extra hours since my husband was home. Contrast this to my neighbors (student husband with stay-at-home wives) who got Medicaid (=free babies), Food Stamps (and SNAP is very generous to zero income families), Tax “refunds” (despite the fact that they didn’t pay any taxes due to having zero income), nearly free rent. They all claimed to be poor yet they frequently ate out and took nice vacations during Christmas, Spring Break, and the summer. One family on all of the welfare assistance listed above went to California, Jamaica, AND Hawaii in a single year! [Those were vacations, not visiting family vacations.] I personally find it to be dishonest, using another hard working person’s money to help fund your vacations. My parents have worked hard all of their lives and have not visited any of those locations, so why is it okay for those using taxpayer dollars to do it? We freak out about AIG and other large institutions with government bailouts throwing expensive parties but it’s okay for welfare recipients (which is nothing less than a government bailout) to do the same? I think a modest trip to see family is okay, but as a taxpayer who has seen the system used and abused (now these previous welfare families have minimal student loan debt, contrasted to our $400k in loans [yes in-state tuition and on scholarship]). There is no fairness in that. We’ll still have the same income and pay the same in taxes despite the fact that I didn’t use a taxpayer penny for my healthcare, food, etc. I don’t care what people spend their money on but I do care about what they spend *my (taxpayer) money on. I’m not saying that “poor” families can never splurge, but I’ve witnessed that most of these families have a lot of material things that they don’t “need” but claim they do (smartphones, tablets, name brand clothing, manicures, etc.). Ask any nurse or person who works in the hospital: you can almost guess who has Medicaid based on what they have with them in the ER waiting room. Penny clearly does live modestly, though I would certainly say the vacation budget is excessive.

Thanks for sharing your story Penny! I absolutely love your positive thinking and the action plan you’ve laid out. Wishing you and your family much success. Cheers to your blog bringing you extra income in the coming months! xoxo

Well, not sure if our blog is going to bring in any extra income, but we’ll see. I don’t think we’ve made any money off it yet.

I am SO glad to see a post like this! My husband’s a teacher, and I just started my own business, so we’re in about the same boat as you, money-wise. I also have a ton of student loan debt – if I only paid what IBR required of me, I’d have ~$156k “forgiven” by the government by the end too – but that looks like $23,000 in taxes, according to your tax calculator. No thanks.

I’m 100% on board with everything you say – particularly to those people who look at us with lots of student loan debt and refer to us as “moochers” (I’m mainly talking about random Yahoo commenters; don’t know why I subject myself to those boards).

What I find funny, though, is that we pay so much to student loans (and, in yours and my cases, the federal government) yet the government is also subsidizing your food support. (My husband and I don’t qualify for food support). Why doesn’t the government lower student loan interest rates? My interest rate for, of course, my largest loan, is almost 8%. That’s more than our mortgage interest and much higher than my husband’s car loan interest rate. Wtf? Pardon my language.

But maybe if we had lower interest rates, we’d pay off our loans faster, and not have to be on food support in your case, or flat out refusing to buy anything new (my case). Wouldn’t the government prefer to have us all out there, spending money, versus hoarding it to pay interest? I guess not!

These are some good questions you’re raising, Melissa.

Good point Melissa — the whole student loan situation is becoming a crisis. Some of it is based on choices (taking out the loans), but some of it is certainly the system — interest rates and schools that are charging fees completely divorced from income potential. –Rich, from pennyandrich.

While I commend you for your honesty and your strategic decision-making about paying off your loans (I’m doing something similar with a similar amount), I think your view of food support as being willing to accept someone else’s donuts is mistaken. You’re accepting something that really isn’t yours to be taking because you want to pay off your loans faster. I don’t have an issue with people eating out and taking vacations but your acceptance of public support enables you to do that – and I don’t know ANYONE else getting public assistance that can even remotely afford to do that. Other people shouldn’t have to pay for your decision to pay down your loans faster. There are lots of ways of making extra money so you can do that, but taking resources meant for people in desperate situations shouldn’t be one of them. And you sound a bit proud of yourself for doing that. Sadly, I think you may need to go back to the Bible on this one, because it has lots to say about managing money and social support.

Agreed. You/your husband chose to take out those loans, and it’s great that you’re determined to pay them off…as you should be. Taking money from people who truly need it, as in desperately need it, is wrong. You can afford to feed your family and pay onto your loans at the same time from what your numbers show. Your post just sounds so entitled and proud. You’re actually scamming the taxpayers to pay off your loans faster. Not much to be proud of there.

Hi Tara and Gretchen — I’m Rich, Penny’s cousin and the other half of our blog. I’ll try not to repeat an earlier comment I made, but I appreciate your honest thoughts and don’t blame you for airing them. I know Penny was concerned about this reaction.

I’m not sure what I’d do in Penny’s situation, but we’re different people. Maybe I’d be working 3 jobs and missing my family in the process. Maybe that would lead to greater stress and to divorce and child support and so on. If there’s one thing I know about Penny, it’s that her family is strong and her kids will be in a good position to contribute to society. That is a social good that lasts generations.

I will tell you, Penny couldn’t scam anyone if she tried — she’s honest to a fault. We may disagree with some of her choices, but she’s human and a great mother.

Either way, I appreciate your honest reaction. –Rich

To the previous commenter, it’s simply not correct that Penny is choosing to take benefits in order to pay off her loans. She and her family are at an income threshold where they automatically qualify for these benefits. How she chooses to allocate her non-benefit income has nothing to do with her ability to claim benefits. In fact, situation is more analogous actually to an independently wealthy retiree taking Medicare.

Responsible student loan repayment should be lauded. Penny could be allocating her money to less “worthy” causes.

Beautifully said, I have been pondering this all day. The taxpayers are basically paying for their loans. I looked into the food stamps (and I asked this earlier about the Food support phrase, I think the use of that phrase was to mislead), I believe you are supposed to be working to receive this entitlement.

Are you intending to receive food support the entire 10 years? You both are capable of bringing home money and not need to burden tax payers for such an extended time. I understand wanting to stay home with your children. I am just now able to stay home with my children (10 and 5) but my husband now can finally support both of us easily. But before then we worked opposite shifts so only we watched our children. Yes that means one works days and one works nights. No daycare. I didnt want strangers watching our children. Yes it was tough. There were days we were dead tired. But it was that or one of us stayed home and we took in government assistance. We could not morally do that. As we both were fully capable of working. Government help I know is necessary in times of need. Lost jobs. Disability. Etc. But your family chose to take on student loans and chose your husband’s career. Money-wise things didn’t go as you planned. (Plans usually don’t go the way we want, keep that in mind with your current plan) But now you are taking hand outs that could go to someone who actually NEEDS it. Basically you are taking a bail out. If everyone (and a lot of people do) rely on the government to bail them out for their plans gone awry and their mishandling of money then where would we be? Your situation is exactly why people stigmatize people on government assistance. Because people see two adults, four kids and one adult doesn’t work. Your family is low income BY CHOICE.

I used to feel that way about food supplement from the taxpayers…before I ended up needing them myself. I just look at it like helping my neighbors, even the ones I can’t see from my front door. When I was working, someone else got to eat and, as a Christian, I feel good about that. And the taxpayer burden per dollar earned is pretty minimal.

I understand helping people in need. But even the Bible says if anyone will not work, neither shall he eat. There are single moms with several kids working multiple jobs to support them and can not get government assistance because she “makes too much money.” That is a person who NEEDS the money. And she is doing what the Bible says to do, WORK, providing for their own especially those within their own house.

Hey Deb — it’s Rich, Penny’s cousin from our blog. I agree with you in part, and just wrote about how Penny and I are from similar backgrounds and our financial situations are the result of certain choices.

That said, I would also say that I disagree Penny is not a good candidate for aid. Her family is solid, and if she worked a night shift or something, they would certainly be worse off as a unit. In the long run they will be fine and that’s what we want as a society. There’s an argument to be made that it is much, much harder to pull people out of abject poverty than to help people through lean times. Just a thought, but I do appreciate your reaction. –R

Deb. Do you have any idea how much child care costs in America? She would be working to afford to send her children to daycare and that’s it. That’s the sad state of things. Promise you that eventually her family’s tax money will go towards helping other people and we can all be even.

Heather, if you read Deb’ s earlier post, she and her husband worked opposite shifts in order to keep their children out of day care.

Lol, you scared the tar out of me about the Income-Based Repayment surprise when taxes are owed on the forgiven amount! My student loans have continued to grow (metastasize?) since I graduated and I don’t have income to throw at them. My kids and I live with my parents while my husband struggles to grow his business and the kids and I receive food supplements. I, too, want to pay them off in time and I’m finally starting a blog to make good use of my writing skills. Thanks for your honest sharing and I hope God richly blesses you and boosts your husband’s business income so you can pay off your loans even earlier

Thank you so much for these words, Janet. We lived with family for awhile too, when my husband first opened up his business. Good luck and blessings to you as well. 🙂

Thank you, Katy. I was expecting to get some flack for my guest post here on this widely read blog, but it actually hasn’t been as bad I as I was expecting, so I am thankful for that. And I am thankful for comments like yours, so thank you, again. Your words are greatly appreciated.

WOW! JUST WOW! When I was a single mother and HAD to depend on food stamps to feed my daughter, I couldn’t wait to get off and support myself. That’s because I was raised to support myself and my decisions. It’s one thing to do all of this but totally another to BRAG ABOUT STEALING FROM THE GOVT. I guess there is a first for everything and this is the first time I have seen someone with balls big enough to brag about ripping the govt. off in writing. SMH. THIS is why people do without because people like Penney “steal” and there isn’t enough for others who NEED IT. my grandparents worked for everything and was dirt poor and very proud. They didn’t take anything. We are raising 6 kids, 2 in college and 3 are adopted (again, my choice) and it really pisses me off that you feel the need to rub it in hardworking american faces. Someone else’s donuts? It sure would be nice to take my family out for donuts once in a while but we consider that a “luxury”.

That’s what made me so angry. The pride and bragging. They chose to take out the loans, have 4 kids and start a business. Love all of that…but why brag about stealing? (Because, that’s exactly what she’s doing.)

Yes, their choices we taxpayers are supporting. I raised two children, and am working a job post-retirement to finish paying off bills. Never asked for help, and did it without a degree. I worked at “man’s” job to provide for my kids, and they are now wonderful, productive adults. When you really need a hand up, ask, but not for a handout.

You are so right. This is maddening. Let’s be clear, however, she is NOT stealing from the government–she is taking from you, and me and every other tax payer by living in this way. The government has no money of its own. The “government money” she is receiving comes from all of us who work for it and pay taxes. And before anyone tells me she pays taxes too–no, she doesn’t. She has said that she gets Earned Income Credit back for her big tax “refund”. That means that not only does she NOT PAY income tax (they get back everything that they pay in during the year on payroll taxes), but she gets thousands more “back” that she never paid in. That comes from all of the rest of us who DO truly pay taxes. And she is getting food stamps/SNAP benefits, which means the family is also able to get several other benefits, such as Medicaid.

There are people out there who are truly in need–her family is not among them. They make enough to live modestly. But then why should they–they are “entitled” to your/our money for which we worked.

I’m as liberal as they come and certainly believe we all belong to each other. That being said, in my opinion, this is scamming. You made choices in your life – chiro loans, 4 kids, SAHM. Those choices are YOUR obligation to pay for, not ours. SNAP is supposed to be temporary help for families in need to assist them in becoming self-sufficient. It’s not meant to be relied on for years by families enjoying lifestyles they can’t afford. What you’re doing is a red-ribbon-wrapped gift to all of the anti-government haters who rage on about welfare queens. It may be legal, but it’s an abuse of the system.

Agreed.

Agree and using the phrase “food assistance” for welfare/food stamps/snap benefits is an interesting twist. Choices and consequences, you made specific choices, student loans, 4 kids, SAHM, and now you want someone else to subsidize those choices. Not cool……

My faith Is being restored by those that worked, or are working themselves out of debt. Penny, I’m sure you are doing what you are allowed to do, but this just shows how wasteful the government is with our tax dollars.

I am a self-employed single mom with a special needs kid. I have massive student loans and have struggled greatly taking care of him and growing a practice all on my own, at times I would have certainly qualified for assistance. I am very liberal and support the existence of social programs for people in need. But this is disgraceful- you don’t have “need.” Read what I am writing: you don’t have need, you have “want” and are gaming the system so that other people are paying for it. Other people’s tax dollars are funding your food stamps and earned income credit, while you deliberately under-earn and use the earnings of others to pay loans you voluntarily incurred, rightfully owe, and will reap the rewards of as your husband’s practice grows. Shame on you.

Hey Robin – I understand your sentiments. I disagree that Penny is deliberately under-earning. I know her. She has made a choice, sure, to stay home with kids, prioritize family, and so on. I don’t even agree with every choice. That said, the system as currently constructed sees Penny as qualifying for assistance, that’s not really up for debate without new legislation. It’s great that you didn’t accept assistance, but you were well within your rights to do so.

Again, I completely understand what you’re saying. If I didn’t know Penny and her complete lack of a dishonest bone in her body, I might even agree. But I think the conversation is important. In this country, we want the poor to be VERY POOR. And we want people to succeed, but to be TOO SUCCESSFUL. I see this all the time. I just think we need to find a new way of talking about it.

–R

My entire career is based on maximizing opportunity in systems. I help people who are at their worst, financially. There is nothing morally right about this. They pay nearly $2k/mo to student loans from money that other people earn, when they could pay their own bills by accepting responsibility for their debt, extending their repayment schedule, and living within their actual means. I made a choice to be a stay at home mother who worked part time for years, when my son was first diagnosed. I could have worked more, but I chose not to. I never asked anyone to pay for that decision for me. I lived within my means instead. Feeling entitled and actually BEING entitled aver vastly different.

I don’t disagree with much of what you’re saying. The part I’d challenge is the assertion that you know exactly how Penny feels. She put herself out there with this blog post, fully aware that there would be some angry responses. But let’s not assume that one post can express all the complex feelings she has about her situation. She is not a proud or entitled person — she’s humble and generous and feels strongly about helping others and paying her debts. How many people in her situation would give to charity or pay $1k a month on loans? I’m not saying these are perfect choices, but they indicate the kind of person she is. She has shown — to me, at least — a willingness to think about her choices and question them. But we don’t persuade people to new courses of action by angrily telling them how they feel, we persuade through conversation. Hey, I disagree with her about a lot of things, but our blog is built around honest and open conversations, and I’m glad Penny has the guts to talk about this openly. Plenty of people are in her situation and won’t speak honestly out of shame.

“Out of shame” is exactly right. Enabler. And you know it, deep down.

Best of luck to all of you.

Rich, how many of us would love to give at Penny’s levels? We can’t, and we wouldn’t take from taxpayers to be able to.

Well-stated!

Penny,

Thanks for sharing this story. I really debated about even posting on this, as I am sure it will upset others on here. As someone who is wildly liberal in so many situations and trying everyday to have empathy for others, I am really struggling to get on board with your idea of finance, life, and how you are managing everything. I do think you are also not responding to dissenting opinions, instead confirming your bias of how you are operating.

First off, I am sure you are an amazing mother to 4 kids. I know that being a SAHM is a demanding job that is harder than most give it credit for. I also understand that you working would create more income, but daycare would eat that up instantly.

I also commend your husband for wanting to start his own business. I always admire people that will go back to school to pursue their desired careers.

All that being said, I just can not get rid of this crazy feeling I have for your family being able to afford three vacations, own a home, donate over 10% to charity, and have a personal CPA do your taxes. I can even get on bored with being human, and being able to shop at Target, Home Depot, and Spend on Christmas for your kids. I never want to put truly poor people down and tell them they can’t do these things that quite frankly make them feel human.

In your current situation I also agree with others that you are playing with fire every single day. You have no insurance to cover any accident for you, your husband, or children. I wish you both luck in that no accident forces you to a hospital or graveyard, as that would wreck yours and your children’s futures.

There are so many expenses in here that so many people can’t possibly make, even on foodstamps. You have an Imac, repaired a camera for $249! I can find you 100 cameras that cost wildly less! There seems to really be no effort to live frugally now to enjoy a better life later. The attitude seems to be keep living now, hope that things work out perfect with life, and if not the government will backstop you.

You also don’t mention health insurance costs, but it seems similar in that you probably have subsidized health care, yet still afford orthodontics.

I think the laissez-faire attitude towards your actual risk, debt load, and carefree attitude towards taking foodstamps while enjoying a non-poor lifestyle is what really upsets me. I feel your church/other organizations would understand your inability to tithe for a few years, allowing you to take care of you family and better your future. I feel you are a great woman of faith that would return to paying your time and money in the future when you earned more.

I also think you could cut back in other places to create a better future and have investments/retirement savings. Hopefully your husband’s job makes millions, and you can live great in the future, but if not I think the outlook is not good at best.

You don’t mention the amount you take in from food assistance, but I feel like if you looked at this honestly, you would find you could feed your family, not take assistance, and still afford your debt payments. It would require sacrifice sure, but I think the important things that you value like family and staying home would still be there.

I guess I kind of wrote a post here, but hopefully my message comes across without being an angry internet user. I just feel upset when I see people that don’t mind living off assistance when really it isn’t ‘needed’. I wish you the best of luck in shoring up your finances, but I do hope you look at this honestly, and realize that maybe you are using more assistance than you truly need.

-Cameron

Hey Cameron — I’m Rich, Penny’s cousin and co-author of our blog. Thanks for your thoughtful comment — it’s a great example of disagreeing without being nasty.

I’ve replied to a few other comments and I’ll try not to repeat myself. I agree with your assessment of risk here, and I think reasonable people could debate the line items in anyone’s budget. All fair.

Speaking of fairness … I think a lot of the uneasiness with welfare and taxes and assistance all comes back to the idea of fairness. It doesn’t seem fair. People who pay high taxes (like me) don’t like it, and don’t like how the money is used. People who can’t get ahead can’t stand hearing about rich people complaining about taxes! Student loans are unfair, schools are unfair, etc etc.

I actually agree — the system can’t be fair for everyone. It’s a big, imperfect system.

But when I look at the big picture, and I know what I know about Penny (her honesty, her desire to do the right thing, her generosity toward others), I can see many positives even if maybe I’d do things differently. Would she be wise to just turn down assistance that she qualifies for? Probably not. Would it be better if she worked night shifts and became an irritable wife and tired mom? Probably not. Would it be better for her to just ignore her loans and take on investments, and wait for the entire loan to be “forgiven”? Nah.

In the big picture, her family will stay together, get an education, and be healthy. We probably aren’t looking at generations of poverty here, and that’s the overall goal of the system with all its imperfections.

Again, I agree with many of your points but mostly I appreciate humanizing the discussion. Rich people aren’t always selfish, poor people aren’t always lazy, and the system isn’t evil. There will always be areas for improvement but the only way to get there is through honest conversation. Thanks for that, Cameron.

–Rich

Rich, I have seen you defend Penny all day, as most family members would, but she is not honest she is scamming the government and the citizens. However, I do agree that this is also our government’s problem too. From what I have read she should have been out of ‘food support’ over 5 years ago.

I am on spousal support and cannot work outside the house and I haven’t been on vacation in over 10 years. Why, no money. No credit card debt either. I am not entitled to it. So many think they are entitled to it all.

True, I’m defending her in part because she’s family. I don’t agree with all of her choices, and I’m up front about that on our blog. But I think it’s important that we have the conversation — to learn and try to understand, to let people speak. Many people in her situation wouldn’t try to share for fear of being shamed, and how would anyone learn from that?

I’m willing to debate all these choices all day. However, it’s quite another step to assume that she’s doing something illegal, or that she’s a scammer, or that she’s entitled, or to ascribe certain motivations and feelings to her. I get the same thing in reverse when people find out I make a lot of money — I must be selfish and greedy and so on. I guess what I’m saying is we need to learn to have conversations about these topics without going to the darkest places right away.

So again, I don’t defend all of Penny’s choices, but I’m a staunch defender of her willingness to tell her story. I know it wasn’t easy for her to do. Let’s talk about what it’s like to be rich and poor in America and persuade each other on better ways of going about it. Thanks, as always, for the honesy –R

Rich,

My husband and I gross about the same as you do. We do pay more in taxes, we don’t have any debt other than our mortgage (which is way below what would be “acceptable” for our income), we work hard to pay cash for everything (including replacement vehicles, house repairs, etc), we give away over 10% of our income every year, and since my husband and I both work our two kids are in day care.

Finally to my point, we’re not in a position right now to take vacations yet our taxes are paying for other families to go on vacation. I don’t think they’re “scamming the system” by taking the food assistance but they are choosing to pay less on the loans (that seem to have been a poor choice as his business will take 10 years to pay off them off so the ROI is terrible) by making the other spending choices they’re making. I also feel strongly that taking the food assistance is definitely not the same as the mom giving her son donuts.

There are plenty of people who have to forgo luxuries like new computers and family vacations in the short-term to be financially independent. It makes me sad that that does not seem to be her goal. And honestly it frustrates me to know that my taxes are paying for someone else to get to do the things that I currently feel I can’t afford to give my own family.

Precisely- I agree wholeheartedly.

And Rich, your endless defense of Penny (who appears to have understandably gone silent here) might be admirable from your position of love and concern for her, but it’s not actually helping. She might be more *irritable*, you say, if her family gave up government assistance and had to tighten their belts more, thereby endangering her families happy future together? The real post would be how to stay together with grace and love when your choices lead you down a difficult path.

Maybe instead of the silence (Penny) and defensiveness (Rich), it would be a good time to reflect, pray, and reexamine some choices that have been made? Listen to what your friends and neighbors on here are saying- it’s not an attack, but rather an eye-opening education that you can pass on some day to someone else, all the while setting an example for your children and those around you of honest self- sustainability.

Hey Lin — I appreciate this and believe me, I’m listening. I really have nothing to be defensive about. I’m completely self-sufficient and I’ve told Penny myself that I’d do certain things differently.

Here’s the difference: When I disagree, I tell her in a civil way and I try to listen to what she’s saying even if I don’t like it. When I disagree with commenters, I do the same. I don’t assume that there’s evil intent involved. There’s a way to do this without making people into enemies, right?

I understand the feeling of unfairness because I pay tons of taxes myself. Loads of taxes. For the most part, I don’t like the way my tax money is used. National debt. Bank bailouts. Etc.

This idea that Penny should voluntarily give up assistance that she qualifies for, because some people think it’s unfair, is misleading. How many people out there qualify for tax breaks, refunds, mortgage interest deductions? Is anyone sending that money back to the Treasury because they don’t really need it? Should we all reject our standard deduction, because, well, we can afford a computer, so it would be immoral to accept the tax system the way it is? I don’t think so. The tax benefits that one qualifies for and how one spends their money are 2 quite different matters.

Penny’s largest spending categories are Student Loans, House Payments, and Donations to Charity. I actually think she should stop giving to charity for a while. At the same time, I can’t accuse her of being selfish without taking this into account.

Personally, I think this conversation is helpful. We don’t agree on everything, not even close. But this is what we do on our blog: we talk about the way we spend money and pursue happiness, and we’re totally open to hearing about how others do it. I have yet to see a budget I completely agree with. Except for mine, ha.

Rich, how many of us would love to give at Penny’s levels? We can’t, and we wouldn’t take from taxpayers to be able to.

Cameron, excellent reply. I bookmarked the SSDD link.