Liberty Healthshare Review Update June 8, 2022 – I personally used Liberty HealthShare for the birth of my daughter in late December of 2021. All of my medical bills were paid quickly and I am happy with the service that I received.

Liberty Healthshare Review Update May 20, 2024 – My husband had a minor surgery this year and it was paid for with no problems as well.

Okay, okay, hear me out first. I want to start out this Liberty HealthShare review and state that this is not a political post, at all. Seriously. This also isn’t a sponsored post or anything like that. This is my Liberty HealthShare review and my research on a health care sharing ministry, as I want to help others find alternative forms of health insurance in case they need it. I did. If you are looking for Liberty Healthshare reviews, then here is my opinion.

I first heard about health sharing ministries about a year ago. I had no idea that they existed, but I thought it was an interesting concept. I didn’t look into it any further because I already had health insurance.

Then, in late 2015, I found out that I had no realistic health insurance options. I didn’t want to pay the penalty for not having health insurance, and I also didn’t want to go uninsured.

See, for full-time RVers, health insurance companies are fairly strict.

Some health insurance companies won’t cover you once you travel away from your state. If they do cover you when out-of-state, they usually require that you at least live full-time in your home state. As RVers, while we do have an address, it is technically not where we live full-time, so we did not want to have to deal with a health insurance company possibly voiding a medical expense if they found out that we were trying to get around this loophole.

Plus, the only policy that we qualified for (in our state) had an astonishing deductible of $39,000 for an out-of-state medical expense. And, as full-time RVers, we are excluded from the majority of policies anyways due to the loophole as described above, so that just didn’t work for us.

Paying a high monthly health insurance premium that comes with a $39,000 annual deductible, and the fact that any of our claims would probably be voided because we are full-time travelers, made this decision a no-brainer.

We obviously had to find something else.

Related blog posts if you’re interested in this Liberty Healthshare Review:

- 30+ Ways To Save Thousands of Dollars a Month

- 75+ Ways To Make Extra Money

- How To Take A 10 Day Trip To Hawaii For $22.40

- The $20 Savings Challenge

So, in January of 2016, we started a membership with Liberty HealthShare. We filled out an application, they approved us, and we even had a medical expense in January that they covered. We NEVER have medical expenses, so it was just a coincidence that we had a claim only six days after we were approved.

And, they covered that claim.

My Liberty Healthshare review:

So, what is a health care sharing ministry?

According to Healthcaresharing.org, “a health care sharing ministry provides a health care cost sharing arrangement among persons of similar and sincerely held beliefs. HCSMs are operated by not-for-profit religious organizations acting as a clearinghouse for those who have medical expenses and those who desire to share the burden of those medical expenses.”

Members of a health sharing ministry pay a monthly share with an agreement to help one another in the risk-pool by covering medical expenses.

The positives of a health care sharing ministry.

The positives of health sharing ministries include:

- Monthly costs that can be much less expensive than traditional health insurance.

- Lower annual deductibles.

- No in-network requirements, so you can go to any doctor, hospital, etc., that you wish.

Also, being a member of Liberty HealthShare exempts you from paying the penalty for not having health insurance.

How much is Liberty HealthShare?

For the three of us, we pay $874 each month.

With this monthly share, “Up to $1,000,000 (per incident) of fair & reasonable eligible medical expenses are shareable after AUA has been met.”

They even have plans for as low as $89 per month.

You can find all of Liberty HealthShare’s options here.

The downsides of a health care sharing ministry.

Now, health sharing ministries are definitely not perfect. As with most things, something this good must have negatives.

Liberty HealthShare is not traditional health insurance, which means:

- They are under no requirement to cover your medical expenses.

- You cannot deduct Liberty’s monthly costs from your business taxes.

- You cannot contribute to a Health Savings Account.

- Pre-existing medical conditions are not covered until years later.

Health care sharing ministries all have some sort of ethical rules that you must abide by such as no smoking, no drinking, and so on. If you incur a medical expense due to something that is against their policies, there is a chance that they will not cover it.

Lastly, I want to repeat this again, the biggest caveat is that there is no guarantee that a health sharing ministry will pay a medical expense. This is because they are not governed under the same laws as health insurance companies due to the fact that they are not considered health insurance.

Related: Do you need travel medical insurance if you travel long-term?

Liberty HealthShare review

First of all, leaving traditional health insurance and joining a health sharing ministry was a difficult decision for us. We’ve always had “normal” health insurance, and we don’t know many people who use Liberty.

However, we didn’t really have a choice.

We even used an RV health insurance broker to see if they could find us anything, which they couldn’t. It was either be completely uninsured or go the health care sharing ministry route.

I will say that I haven’t regretted this decision one bit. So far, I have had no problems with Liberty HealthShare. They have covered one wellness visit as well as an ER visit. It was pretty easy in both cases- they just took my Liberty HealthShare card and didn’t have any questions. Liberty HealthShare didn’t have any questions either.

Liberty HealthShare does have a set of guidelines (which you can find here) that they ask that you follow. But, they accept customers of all faiths, lifestyles, backgrounds, and sexual orientations.

Here are links to Liberty Healthshare’s rules on other questions you may have:

- Liberty Healthshare pregnancy – Maternity & Membership: What to Expect

- Frequently Asked Questions

I will make sure to keep this Liberty HealthShare review updated in case anything happens, especially if my opinion were to change in the future.

How did I hear about this health care sharing ministry?

There were two main people who influenced my decision to join Liberty HealthShare. This includes Holly and Choncé. Both of them are Liberty HealthShare members, and here is what they have to say about the company:

We joined Liberty HealthShare in 2014 after seeing our premiums double due to the Affordable Care Act. So far, we have seen tremendous value with our plan, and all for a price that is half of what we would need to pay for health insurance. And, instead of having a $12,000 or $13,000 deductible with Obamacare, we have a $1,500 annual out-of-pocket max. – Holly Johnson at Club Thrifty, Why We’re Joining a Healthcare Sharing Ministry

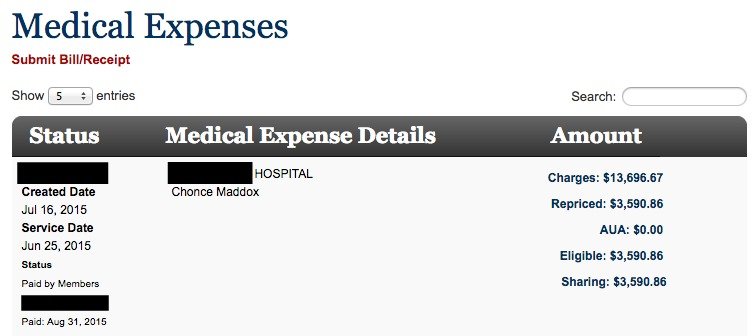

I’ve been using Liberty HealthShare for about a year and a half now. At first, I was hesitant to try it, but health insurance premium quotes were very high for me so I knew I didn’t have much to lose. Now, I am so happy I gave it a try because I like how I can visit any doctor I want and Liberty has really stepped up to share my medical expenses so I don’t have to cover them out of pocket. Last year, I had to have a surgery done which totaled around $13,600. Liberty HealthShare repriced my medical bills to about $3,500 and shared the entire expense. Having surgery is scary enough on its own, but I felt peace-of-mind knowing I wasn’t going to be bombarded with tons of unnecessary medical expenses afterward. Liberty HealthShare is still growing and the team is always open to hearing suggestions and trying to improve each member’s experience. I like how one team member offered to call a doctor I was interested in seeing to explain to them what a health sharing ministry is and ask if they would accept me as a patient. – Choncé at My Debt Epiphany, Putting My Health First: A Review of Liberty HealthShare

Choncé was also kind enough to share a screenshot of how Liberty HealthShare paid the entire expense of a surgery she had last year.

If you’re interested in Liberty HealthShare after reading my Liberty HealthShare review, please send me an email at michelle@makingsenseofcents.com, and I can put you in touch with someone at the company. They will explain it further and answer any questions you have..

How much do you pay monthly for health insurance or an alternative? What do you think of health care sharing ministries?

Disclaimer with this Liberty HealthShare review: You should always do your own research when it comes to a big topic such as choosing health care, a health care sharing ministry, and health insurance. This is just my opinion and review of Liberty HealthShare, but you should remember that I am not a health care professional or expert.

Leave a Reply

Thanks so much for posting this, Michelle! I was laid off from my full-time job last week and health insurance has been one of my biggest concerns. I’ve browsed healthcare.gov for Tennessee, but I’m not pleased with the rates I’m seeing. It’s great to know about another reputable option.

I’m so sorry that you were laid off Kate. I had no idea!

Yes I too am looking into Liberty share because I have just recently been informed that the government assistance that I received on Oboma care is taxable income. Was not made aware of it up front or perhaps I missed it. I was dropped by United health care after less than one year because the pulled out of the program. Liberty is looking better by the minute as I am self employed.

Be careful, I used liberty health,and 5 months later had a heart attack, on a 100,000 bill they payed $6,000. that’s all,

Did they state why that’s all that they paid?

Frank, Why wouldn’t they pay?

Interesting concept and interesting write up about your experience. I also find it very interesting that finding insurance can be difficult being a RVer. It totally makes sense, but is also not something one would instantly think of when deciding to live in a mobile unit.

Yeah, I had no idea. I had heard it was difficult, but it’s definitely more difficult than I originally thought, haha!

I had never heard of this concept before- so interesting! Is Liberty Healthshare one of the bigger providers out there? Since these ministries are under no obligation to actually pay out, it sounds like you’d definitely want to pick one with a lot of paying members.

I learn something new every day on here; great article!

I believe there’s only 3 main ones, so yes.

Very interesting; I’ve always been curious about these healthcare sharing ministries. It sounds like a great option for you & I appreciate the information and your experience. Never thought about the difficulty of coverage for full-time RVers. Do you think the right to reject coverage is in part their way of guarding against people over-using the sharing system?

No, I think it has a lot to do with their values. They don’t want to cover people who get into a drunk driving accident, those who are risky, etc.

My husband works for the state, so our health insurance is much more affordable, though the premiums have been increasing quite significantly in the last year. We pay about $188/month to cover our family of 6 for a high-deductible health plan (the year before we just paid $67/month!), and contribute an additional $150 monthly to our HSA. On top of that, the state contributes $2250 a year into our HSA. Our deductibles are a little high, $2750/individual and $5500 for family, but that’s OOP max. All of this will probably change, though, in the next year as the state looks at more premium increases and decreases in contributions to employee’s accounts.

I have looked at healthcare sharing ministries before and I think that they are a good option for people who don’t have access to a good plan. But one that I looked at (Samaritan) seemed to have a cap on the total amount it would assist with. I think it was $250,000, which may seem like a lot, but if you were in ICU for a year or got cancer, that would be gone very quickly. I also don’t like the litigative side of it in that they aren’t liable to pay for any of your expenses. You would think that if you are paying a certain amount, they should be liable for something.

I know many people use these ministries and are happy with them. With premiums rising and more people considering going to them, it will be interesting to see if the restrictions on them change in the years to come. Obamacare is dependent on participation on the health insurance markets – if people choose other options, it would reduce that participation.

Yes, the fact that they can decide what they will cover somewhat scares me. I have no other choice since no one else will cover us, though, so this is better than not being covered.

For anyone interested, Samaritan Ministries offers unlimited need sharing (no cap) if you join Save to Share, which is their very low cost add-on to their base plan and designed specifically for those expensive cancers, heart issues, etc. Anyone wanting full “Coverage” for anything that could go above the $250,000 base amount would want to be part of that (and I would highly recommend it, it’s very low cost for tremendous peace of mind). We have been Samaritan members for several years and are very happy with it. 🙂 It’s true there is no contract, but they also operate with the singular purpose of helping members instead of trying to get profit from them. After 20 years of successfully having 100% of qualifying medical bills met we felt they have proved their viability and the contract issue became moot. On the other hand, if we had insurance we could pay more than $30,000 next year (premiums and huge deductible) before insurance would pay a dime beyond our “free” physicals. I am so thankful that healthcare sharing ministries exist and that most are ACA exempt (that would include Samaritan and Liberty).

I recently joined Samaritan and have been excited about the cost and the entire Sharing concept, Christians helping each other with med expenses. I also liked the fact that each members share goes directly to the person with a need. However I just heard about Liberty tonight and I like the fact that those share amounts get paid to the provider vs. the member who has a claim. I guess there is some risk that a member with Samaritan could receive payments and not pay the provider which could hurt Samaritan. Of course with this being a Christian share program, we would hope a member would not do this.

The one thing I have been concerned about with Samaritan is regarding pre-existing conditions. I have high cholesterol and high blood pressure. I have not been able to get Samaritan to tell me if these conditions are considered pre-existing if I were to have a heart attack or stent required. On the other hand, Liberty has a program for people like myself in which a coach is assigned in order to improve your health for a year. You are required to stay in touch with the coach at least once a month to improve your lifestyle and your health situation. Then you graduate after you have improved by the end of the year. So with liberty a person like myself knows where you stand and have the opportunity to improve yourself while participating fully in the share program. While the out-of-pocket for my wife and I would be $600 with Samaritan and $1000 with liberty I’m thinking Liberty might be the better choice for us. Just my thoughts. I think any of the 4 major Share programs are much better than the Obamacare option. Thanks for your post and opening up this discussion.

I am so glad that you posted this! I left my full time teaching job in May and I was the insurance provider. Before making the decision for me to quit my job, we researched these options. I think we have settled on another healthcare sharing plan but I will certainly compare it to this one. I will be honest. It is a little scary to me. I think because it is just not the “norm.” I appreciate your honest review.

Yes, I agree, it can definitely be scary! We have been happy so far – it’s a hard decision.

Thanks for sharing the details of your experience, Michelle! We are thinking ahead to retirement – health insurance premiums could be a killer in early retirement. This may be a viable option for us too. I appreciate the information!

Welcome!

I’m intrigued by this concept-I’ve heard of health car sharing ministries but never known any details about how they work. Since this isn’t technically health insurance does it still count in waiving the penalty for Obamacare health insurance requirements?

There is no penalty if you are a member of one of the grandfathered ministries. Liberty is one of them, so I do not have to pay the penalty.

Awesome!

That’s awesome! I’m glad you got a good deal. My Mom uses another HealthShare type insurance provider. It makes a lot of sense if you are self employed and can’t afford Obamacare!

Thanks! This choice didn’t have to do with money, though. As full-time travelers, we didn’t qualify for anything else.

You say that you have no other options because you are full-time travellers. However, I’m aware of a frw providera that cover digital nomad types, like World Travellers. I know they’re premiums go up if you include US coverage, but did you look into insurance plans designed for travellers?

I was referring to traditional health insurance when I said that there were no other options 🙂

Yes, I did look into plans that were designed for travelers, but almost all of them meant that you had to pay the health insurance penalty.

Ah, I forgot they don’t cover the penalty! My apologies. Also, I hadn’t heard of these health shares before this, so thanks for spreading the word!

Yeah, it stinks that they don’t cover the penalties. We are happy with Liberty, though! 🙂

are you still happy w liberty health share? have you needed to use it for a big expense? Debating if i should do Liberty or CHM for my family.

I am still happy with Liberty. We’ve used it for a few expenses, but nothing over $2,000.

My understanding is that with Samaritan and Christian Healthcare, you have to pay the first $300 and $500 of a bill respectively. Versus with Liberty, you pay a $1500 “deductible” then 100% is paid. If we only end up having small sick visits and wellness visits, then with Samaritan and CHS none of our bills will actually be shared/paid because they’ll be under $300/$500.

Emilee, you are almost right. With Liberty the “deductible” (annual unshared amount) is $500 for singles, $1000 for couples, and $1500 for families.

I have never heard of a healthshare before. This is great information! When we inevitably start traveling this will be something I will look into for sure!

Welcome!

I’ve noticed two things the past three years: almost everyone I talk to who has to shop in the exchanges has found them unaffordable, and insurers are losing hundreds of millions of dollars on these already unaffordable plans. My company recently left most of the exchanges after losing half a billion dollars (with a B!) on our plans.

Naturally people are moving to health sharing ministries and it really has found the ultimate loophole: no one takes risk. Or collective risk, I should say. I’m just surprised the government hasn’t intervened yet. The fact that people who previously had cancer or other conditions is what keeps the costs down. It’s a good setup for people who are forced to shop in the exchanges, so I’m glad you are taking advantage of it.

Mandatory disclaimer that I speak for myself and not my employer…

I was hoping that you would comment DC! That’s crazy that half a billion dollars was lost by your company!

Being with a health care sharing ministry does somewhat scare me at times because of the unknown. However, like I said in the post, I don’t have a choice because no health insurance company will cover us as full-time travelers. I do wonder if health insurers will ever change that in the future.

It seems like another advantage is that the unknown might drive you further to an even healthier lifestyle. When all these changes in health care started happening, my husband and I resolved to not need it. I know it’s a lofty goal but our personal health did a 180. DH lost 50 pounds, we got more active and we stopped eating crap. We never get sick now and that’s been since the ACA was passed.

I had no clue about this. Very interesting! We are paying so much for insurance now that my husband and I are both independent. (I paid $0 in premiums at my prior employer.) And from last year to this year our premiums jumped about 30%. Yikes. At least we can deduct our premiums from taxes.

Chonse at My Debt Epiphany said “Last year, I had to have a surgery done which totaled around $13,600. Liberty HealthShare repriced my medical bills to about $3,500 and shared the entire expense.”

What exactly does repriced mean?

Liberty got the hospital to discount the bill to just $3,500, and then that’s all that Liberty had to pay. This is so that everyone saves money. Hospitals usually inflate bills.