Liberty Healthshare Review Update June 8, 2022 – I personally used Liberty HealthShare for the birth of my daughter in late December of 2021. All of my medical bills were paid quickly and I am happy with the service that I received.

Liberty Healthshare Review Update May 20, 2024 – My husband had a minor surgery this year and it was paid for with no problems as well.

Okay, okay, hear me out first. I want to start out this Liberty HealthShare review and state that this is not a political post, at all. Seriously. This also isn’t a sponsored post or anything like that. This is my Liberty HealthShare review and my research on a health care sharing ministry, as I want to help others find alternative forms of health insurance in case they need it. I did. If you are looking for Liberty Healthshare reviews, then here is my opinion.

I first heard about health sharing ministries about a year ago. I had no idea that they existed, but I thought it was an interesting concept. I didn’t look into it any further because I already had health insurance.

Then, in late 2015, I found out that I had no realistic health insurance options. I didn’t want to pay the penalty for not having health insurance, and I also didn’t want to go uninsured.

See, for full-time RVers, health insurance companies are fairly strict.

Some health insurance companies won’t cover you once you travel away from your state. If they do cover you when out-of-state, they usually require that you at least live full-time in your home state. As RVers, while we do have an address, it is technically not where we live full-time, so we did not want to have to deal with a health insurance company possibly voiding a medical expense if they found out that we were trying to get around this loophole.

Plus, the only policy that we qualified for (in our state) had an astonishing deductible of $39,000 for an out-of-state medical expense. And, as full-time RVers, we are excluded from the majority of policies anyways due to the loophole as described above, so that just didn’t work for us.

Paying a high monthly health insurance premium that comes with a $39,000 annual deductible, and the fact that any of our claims would probably be voided because we are full-time travelers, made this decision a no-brainer.

We obviously had to find something else.

Related blog posts if you’re interested in this Liberty Healthshare Review:

- 30+ Ways To Save Thousands of Dollars a Month

- 75+ Ways To Make Extra Money

- How To Take A 10 Day Trip To Hawaii For $22.40

- The $20 Savings Challenge

So, in January of 2016, we started a membership with Liberty HealthShare. We filled out an application, they approved us, and we even had a medical expense in January that they covered. We NEVER have medical expenses, so it was just a coincidence that we had a claim only six days after we were approved.

And, they covered that claim.

My Liberty Healthshare review:

So, what is a health care sharing ministry?

According to Healthcaresharing.org, “a health care sharing ministry provides a health care cost sharing arrangement among persons of similar and sincerely held beliefs. HCSMs are operated by not-for-profit religious organizations acting as a clearinghouse for those who have medical expenses and those who desire to share the burden of those medical expenses.”

Members of a health sharing ministry pay a monthly share with an agreement to help one another in the risk-pool by covering medical expenses.

The positives of a health care sharing ministry.

The positives of health sharing ministries include:

- Monthly costs that can be much less expensive than traditional health insurance.

- Lower annual deductibles.

- No in-network requirements, so you can go to any doctor, hospital, etc., that you wish.

Also, being a member of Liberty HealthShare exempts you from paying the penalty for not having health insurance.

How much is Liberty HealthShare?

For the three of us, we pay $874 each month.

With this monthly share, “Up to $1,000,000 (per incident) of fair & reasonable eligible medical expenses are shareable after AUA has been met.”

They even have plans for as low as $89 per month.

You can find all of Liberty HealthShare’s options here.

The downsides of a health care sharing ministry.

Now, health sharing ministries are definitely not perfect. As with most things, something this good must have negatives.

Liberty HealthShare is not traditional health insurance, which means:

- They are under no requirement to cover your medical expenses.

- You cannot deduct Liberty’s monthly costs from your business taxes.

- You cannot contribute to a Health Savings Account.

- Pre-existing medical conditions are not covered until years later.

Health care sharing ministries all have some sort of ethical rules that you must abide by such as no smoking, no drinking, and so on. If you incur a medical expense due to something that is against their policies, there is a chance that they will not cover it.

Lastly, I want to repeat this again, the biggest caveat is that there is no guarantee that a health sharing ministry will pay a medical expense. This is because they are not governed under the same laws as health insurance companies due to the fact that they are not considered health insurance.

Related: Do you need travel medical insurance if you travel long-term?

Liberty HealthShare review

First of all, leaving traditional health insurance and joining a health sharing ministry was a difficult decision for us. We’ve always had “normal” health insurance, and we don’t know many people who use Liberty.

However, we didn’t really have a choice.

We even used an RV health insurance broker to see if they could find us anything, which they couldn’t. It was either be completely uninsured or go the health care sharing ministry route.

I will say that I haven’t regretted this decision one bit. So far, I have had no problems with Liberty HealthShare. They have covered one wellness visit as well as an ER visit. It was pretty easy in both cases- they just took my Liberty HealthShare card and didn’t have any questions. Liberty HealthShare didn’t have any questions either.

Liberty HealthShare does have a set of guidelines (which you can find here) that they ask that you follow. But, they accept customers of all faiths, lifestyles, backgrounds, and sexual orientations.

Here are links to Liberty Healthshare’s rules on other questions you may have:

- Liberty Healthshare pregnancy – Maternity & Membership: What to Expect

- Frequently Asked Questions

I will make sure to keep this Liberty HealthShare review updated in case anything happens, especially if my opinion were to change in the future.

How did I hear about this health care sharing ministry?

There were two main people who influenced my decision to join Liberty HealthShare. This includes Holly and Choncé. Both of them are Liberty HealthShare members, and here is what they have to say about the company:

We joined Liberty HealthShare in 2014 after seeing our premiums double due to the Affordable Care Act. So far, we have seen tremendous value with our plan, and all for a price that is half of what we would need to pay for health insurance. And, instead of having a $12,000 or $13,000 deductible with Obamacare, we have a $1,500 annual out-of-pocket max. – Holly Johnson at Club Thrifty, Why We’re Joining a Healthcare Sharing Ministry

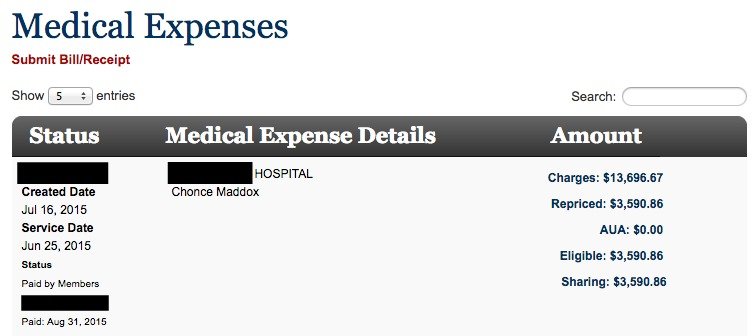

I’ve been using Liberty HealthShare for about a year and a half now. At first, I was hesitant to try it, but health insurance premium quotes were very high for me so I knew I didn’t have much to lose. Now, I am so happy I gave it a try because I like how I can visit any doctor I want and Liberty has really stepped up to share my medical expenses so I don’t have to cover them out of pocket. Last year, I had to have a surgery done which totaled around $13,600. Liberty HealthShare repriced my medical bills to about $3,500 and shared the entire expense. Having surgery is scary enough on its own, but I felt peace-of-mind knowing I wasn’t going to be bombarded with tons of unnecessary medical expenses afterward. Liberty HealthShare is still growing and the team is always open to hearing suggestions and trying to improve each member’s experience. I like how one team member offered to call a doctor I was interested in seeing to explain to them what a health sharing ministry is and ask if they would accept me as a patient. – Choncé at My Debt Epiphany, Putting My Health First: A Review of Liberty HealthShare

Choncé was also kind enough to share a screenshot of how Liberty HealthShare paid the entire expense of a surgery she had last year.

If you’re interested in Liberty HealthShare after reading my Liberty HealthShare review, please send me an email at michelle@makingsenseofcents.com, and I can put you in touch with someone at the company. They will explain it further and answer any questions you have..

How much do you pay monthly for health insurance or an alternative? What do you think of health care sharing ministries?

Disclaimer with this Liberty HealthShare review: You should always do your own research when it comes to a big topic such as choosing health care, a health care sharing ministry, and health insurance. This is just my opinion and review of Liberty HealthShare, but you should remember that I am not a health care professional or expert.

Leave a Reply

Long but lots of first hand helpful and specific details…

I have been with Liberty for about 18 months. I have needed to use it more than most this year and can say it is the single best decision I have made. I choose it when I calculated my out of pocket cost for premiums and copays on ACA would be $45K if my daughter was in the ER (likely, she is allergic to nuts) and if we had one other serious episode. Considering I make $52K, that did not seem very “affordable.” So I researched extensively knowing I had to find another solution but I was skeptical at first. I liked Liberty better than Samaritan because they had better tracking on the money and an online portal and Samaritan requires a pastor from your church to sign off on every bill submitted which seemed excessive to me. I also like that Liberty’s statement of beliefs were more inclusive.

So onto my actual experience. In June last year, I was in a significant car accident with both my children. Liberty has been fantastic in paying all of my bills which have been substantial. They have limits like 20 PT visits per year or 12 chiropractic but they waive those limits if the situation warrants it, so I have had probably had over 100 of those visits and they pay. They have even paid for 40+ visits for acupuncture for pain. They paid for my broken teeth to be repaired since it was part of a traumatic injury. I dislocated my jaw in the accident and despite the fact that they say they don’t cover durable medical equipment, they paid for a $1250 retainer and classified it as a “cast” like for a broken arm. So I have found if I just ask for what I need they tend to try hard to find a way to work with me. I also had some other issues and I could go to an alternative medical doctor of my choosing that I previously had to pay out of pocket. Also, despite the fact my son move to Honolulu for a gap year, there has been no issue with paying. With $1000 “deductible” for a single parent family this has been a non issue financially. They have also been great working with my personal injury attorney.

To address a couple of issues I read above:

*The sharing ministries have been operating successfully for 20 years, they can’t say they will pay because they can’t be considered insurance but they do. If they stopped paying, everyone would stop paying monthly and then I feel like I would just be in the same position as when different providers dropped out of ACA and rates went up. Regular health coverage is a risk too and I believe they are more likely to deny charges.

*HSA – I agree it is a bummer you can’t add to an HSA, but it only saves you a few hundred dollars in tax. There is legislation proposed to change that but who knows when it will happen. I have just been using my old HSA money to cashflow my bills. If a doctor won’t bill directly to Liberty (about 50/50) then I ask for the self pay rate and use my HSA card. I submit the bill online to Liberty when I get home, about a 2 min process and I get paid back in about 3-4 weeks. Then I redeposit the money in my HSA and repeat. I will keep my HSA money restocked by the end of the year so I can use it next year, with only $1000 out of pocket it is easy to show at the end of the year that I have replaced all of the funds. Nice way to keep the max money available without upsetting my month budget.

*Preexisting conditions. My daughter’s anaphylaxis was not counted as a preexisting condition despite being a life long condition because she has gone 24 months without a reaction (her longest streak ever, then broken about 2 months after going on Liberty.) My physical therapist had 20 year high blood pressure but they accepted her if she did coaching for 2 months ($80/mo) just to see if there was anything thing she was missing then after 2 months they considered her fully covered even if something goes wrong related to blood pressure, so they do make exceptions in some cases, just ask. Her husband had a stoke and so they accepted him with the normal pre-existing conditions (no coverage year 1 for related issues but covering everything else, $25K max year 2, $50K max year 3, full coverage year 4.) They decided to put him on and keep his old insurance since it is only $100 more per month to add him to LIberty. After the first year, Liberty will allow you to turn in any costs not paid by your other insurance against your $25K…they decided with a $10K deductible on his normal insurance that they could recoup in year 2 and 3 it would be worth the extra $1200 for 3 years to wait out the preexisting condition then drop his old insurance.

*Discounting bills. All providers charge huge rates and all insurance companies pay less, most of the time 60%+ less. I had a $18K follow up visit in the ER plus ambulance. They paid the ER $720 + $300 MRI + $1000 ambulance. The ambulance company accepted the payment. The ER started sending me balance bills demanding payment. Liberty has an email you just send anything you get in the mail demanding payment and they either deny it or pay a bit more if needed. But I never heard another word, it was simple! Also, in the case of my alternative medicine doctor, I paid her regular cash rate $450/hr and Liberty reimbursed my in full. They typically pay less on charges billed to them and pay the full price if you pay at the time of the service. P.S. If you go to Labcorp for testing, tell them you refuse to sign the paper that says they will bill your credit card on file for any amount your insurance does not cover. Also, when they say they can’t bill Liberty (or say you have to sign the other paper) they are lying. Demand to bill Liberty, do not give a CC and do not sign the paper. I had about $60K in testing this year…Liberty paid about $20K, if I had signed the paper, they would have kept billing my card for the rest! Lastly, this discounted billing thing works even for me by myself…when my daughter needed her wisdom teeth out and I found out my ex had canceled her dental insurance. I just went to the oral surgeon and said “I don’t want to do the used car dealership thing. I am willing to pay cash up front but I know that no insurance company pays $3200 for these services. Can we settle on a reasonable and fair cash price?” Within 5 minutes he had talked to the billing lady and they dropped my bill by $1700…just for asking.

A few things to consider about Liberty and a few ways around them:

1. Liberty has very limited coverage for Medications, 45 days max but they have a discount program. I have found GoodRx App has better prices and most drugs are surprisingly inexpensive, just ask you doctor about generic or reasonable options or just ask if they have any samples. They actually charge you less if you pay cash then they bill your insurance. I had one medication for $800 for 20 days, but I looked on GoodRx and the price for cash was $300-$48. I drove an extra 10 miles and paid $48 (whole time standing there feeling like I was doing something wrong, even the pharm tech said “oh, these codes never work” and I said ” well, give it a try and if it doesn’t, there is a number on there we can call to work it out.” No problem, it worked. Even got the same price on my future refills.

2. Liberty does not cover durable medical equipment. Sounds bad but it is pretty small in the bigger picture. Every major city has used medical equipment for sale, so if you need a brace or wheelchair, etc. do not rent or buy full price, check out these used shops. I live at high altitude and need an oxygen concentrator at night. My old insurance used to pay $288 per month to Apria for a high altitude concentrator and I am sure they would be happy to charge me the same. I found a guy on Craigslist (I did check him and his company out extensively) who maintains and sells concentrators to people who have mountain ski homes. I got a used one for $450 that had just been refurbished and calibrated. I have been using it since I switched to Liberty with no problems.

3. Liberty just started requiring preapproval for testing. Just call in for an approval. They are using it as a cost saving measure but they are very reasonable in their approvals. They also cover alot of less standard test that an alternative medicine doctor might order that regular insurance would not so the small extra step is no big deal.

So all in all, I will be an empty nester in a year and Liberty will continue to cover both kids no matter the state they live and they will be able to use the on campus clinic if they want. Also, I will be covered not matter where I wonder. So honestly, I believe Liberty is even a better value than I thought based on my research. My experience and being forced to face a number of unexpected hurdles, I can find no area I feel Liberty has let me down.

I am so glad there is a way to ride out this nonsense in our healthcare system upheaval!

Hi there, Are you still happy with Liberty? Just found that my insurance policy is getting cancelled at the end of the year and thinking about signing up.

Thank you so much for your detailed post! I am signing up this week. My policy (with Medica) through the Market Place is going to nearly double in 2018 from $750 to over $1,200/mo for single coverage. I agree with the statement that our health insurance should not cost more than our mortgage payments!!! Crazy. I had already decided to go with Liberty, but I feel so much more at ease after reading about your experiences and tips. I wish I had listened and taken the advice of a friend who recommended Liberty a year ago during Open Enrollment; I would have saved about $5,500; I could really use that cash to cover other needs as a newly divorced mom of 4 kids trying to figure out how to cover all the bases on time every month.

Thank you so much for the details and a real-life scenario to visualize.

Incidentally, being that you just posted in May of 2017 to say that you were happy with Liberty, I cannot understand while other posters would be asking in August, whether you were still happy with Liberty.

I have been considering Liberty Healthshare for awhile but I guess the fear of the unknown has kept me from signing up. I’m wondering if anyone has signed up with Liberty but kept their “traditional” medical insurance for a period of time until they were comfortable and confident there would not be any issues with Liberty.

Also, we live in a small town (< 20k) and I don't see any Liberty preferred providers in my area. What happens if you see a doctor not in the Liberty "network"?

Thanks to all for the great info.

I’m an early retiree and have been on Obamacare for 2 years (retired at 53). I’ve seen it go up in cost and down in value and choice tremendously. I’ve been researching alternatives for a while now and Liberty is on top of my list. You being a full-time RV’er bring up another consideration – full-time traveling. I spoke with Kim at Liberty and he assures me they will cover me internationally as well as domestically. I may need to pay the expense first and then be reimbursed but that should not be a problem unless it is $$$.

Do you or any of your readers have any experience with Liberty and international travel or living?

I have been with Liberty Healthshare for almost 3 years. I enjoy the low premiums however, I am actively looking elsewhere as trying to get doctors and health facilities to use the card has been a nightmare. We are constantly considered self pay and then I must send in receipts which almost always get rejected because they need more information. My son broke his leg. At first it looked liked it was going to be covered. They “repriced” it and shared it, only to get the balance due later from the hospital for 10,000.00. I am responsible for that amount because remember they don’t have to cover it if they don’t feel like it. I do not recommend this to anyone. I love the concept and it seems great, but paying off a 10,000.00 hospital bill is no fun.

Would you please share why it wasn’t covered? Isn’t there a legal department designed to protect against just this?

Hello Matt,

Not true! Liberty Healthshare will pay but like any other insurance company they need the proper paperwork (1500 universal form, medical notes, etc) to process the bill. I too as a new member 2/1/2017 could not get bills paid at first only to find out that NOT ONE Hospital or Doctor in Southern Oregon considered them an Insurance company so was not even trying to submit my bills to Liberty or provide them the medical notes, 1500 forms or additional information Liberty requested from them and needed like any other insurance company to process our claims! So, I order the 1500 forms and all medical notes for each visit have them mailed to me then upload all of it together to Liberty with the bill and have Liberty send me the reimbursement checks. Year to date everything 100% has been paid about $18,000 total no deductibles or co-pays as all of the visits have been well care including our expensive colonoscopies. I did have some arguments with the hospital’s billing department not providing me what I requested, so told them I would get a christian attorney that I felt because my insurance was christian I was be discriminated against – they straightened up and cooperated with all my requests. But again at first being skeptical I thought I was getting a run around by Liberty only to learn the Hospital’s and Doctor’s billing departments were giving me the run around by not sending me the proper additional information I was requesting on Liberty’s behalf. We pay $299 per month for my husband and I. So far we have paid Liberty $2,691 and they have reimbursed us about $18,000. Liberty said Oregon is the worst State for them to deal with so they have our account flagged to always send the reimbursement checks to me since I am the one submitting the claims and providing them the proper paperwork. I do spend some time uploading the claims, but it is so worth it! Under the ACA our monthly premiums would be $2,400 per month plus $20,000 for annually deductibles to get only 60% covered on bronze plan. We simply could not afford it!!! But we had to get health care now that we are 61…..

PS

Like other insurance companies, Liberty pays 125% of what medicare charges, so I can tell you your hospital bills were excessive and that is why Liberty did not pay all of it first go around. I had this same problem with one of the hospital bills that had a $4, 432 excessive charge, so called the billing dept asked for the self pay discount. They discounted all but $1,000 and then let Liberty know. (Excessive charges are explained in the sharing guideline membership booklet). Liberty explained to me that if you are not stuck with an excessively charged bill they resubmit it to a different dept for processing. I was reimbursed the $1,000 by liberty within 2 weeks.

Another useful real-world example that helps us to visualize exactly how this system works. Thank you so much for sharing real examples.

Thank you this help me make a decision on whether to pay Cobra or not.

Does anyone have any experience with Medishare? Thank you.

I read through your post. While mostly accurate, there is one glaring mistake. You would not have had a $39,000 deductible on a health plan. The law would not allow that. You may want to amend that statement.

It’s what I was told by an insurance company when I was looking for insurance. I was told that because we travel full-time and would always be out-of-state and out-of-network.

There is no English word as “anyways”. The word is “anyway”.

Jen – The people on this forum aren’t seeking grammatical critique. Perhaps you can find value in the time they’ve taken to share their knowledge.

Michelle,

I have been researching this type of offering for our family due to unreasonable deductibles and insurance premiums. Self employment is not a friendly status for reasonable healthcare rates. I thought I read somewhere that the cost for the insurance could be considered as a donation contribution on your personal taxes. I know there is probably limit but maybe it would help offsite some of the cost. Do you have any background regarding this?

Does anyone have real-life experience with Liberty paying on-time issues, trying to compare Medi-Share paying ontime vs Liberty.

I would like to know this as well. I am almost convinced that I should go with Liberty, but I have heard that it is hard to get them to pay the medical bills in a timely manner. Has anyone had any problems with the time it takes to get medical bills paid?

I have had Liberty since Jan 2017. Unfortunate for me I had a gallbladder surgery in July that went wrong and spent 11 days in hospital few ER visits all total over 100,00.00 in Medical bills. My Hospital does bill them directly as a courtesy, which has been nice otherwise I just submit my bills to them. I will say at first it seemed like it was just shy of 90 days but they have since hit around the 45 -60 day payout. I am sure it depends on number of claims being submitted and what is in each bill. They are still processing some claims as needed additional itemization ( I suppose hospital did not send it) but looks as if every single dollar except my 1000.00 deductible has and will be paid. What a relief. I changed from over 1000.00 AFC plan with 15,000.00 dollar deductible. I am much better off with a 299.99/month plan. I am very pleased and they have to date been wonderful to work with. It was worth the leap of faith!

With LHS since Feb 2017. Infected arm in July, ~$4500 in costs. All but $500 was covered. I self-paid and some of the costs came down %92! Probably better than what liberty could do on their own. I called Liberty and they were very happy that I got the good self-pay rates. They went out of their way and repaid me (minus the $500 “unshared” amount) within 3 weeks.

Be organized: call for self-pay rates as soon as you get the bill, if it is less than 50-60% off let LHS deal for you (I made up that %; this is a grey area…). If you don’t self pay ask the dr.s billing dept to send you a statement that includes all procedural codes and immediately scan it and submit to LHS.

Make an excel file for: 1) what was charged; 2) negotiated; 3) paid by you; 4) paid by LHS; 5) bills sent in to LHS; 6) receipts sent in to LHS.

Sounds difficult but except for the self-pay step it is pretty straight-forward. What with premiums 1/3rd the cost of the cheapest high-deductible insurance, and the low $500 “deductible”, I saved ~$5-6K this year.

We have been using a similar bill sharing ministry for about 3 years. We use Samaritan Ministries. The monthly cost is about the same, but the out of pocket is $300 per “incident”. If the discount for paying cash exceeds the $300, then they waive the $300 co-pay. Last year I had a ER visit and a doctor visit totalling several thousand dollars and didn’t have to pay anything out of pocket after the discounts. We have been very happy with them. With Samaritan you send your monthly payment directly to a person to pay their medical bills, not to the company. Not sure if Liberty does that or not. I think they operate a bit differently. I also recently saw that there is legislation being worked on that would allow people who use these ministries to contribute to Health Savings Accounts. Samaritan Ministries is really active in changing these types of laws.

Thank you for this great post on Liberty. Our family made the transition officially last week and we are set to join Liberty as of January 1 when our current plan expires. We were naturally a little hesitant but are hopeful this will be the right choice for our family. Thanks again for providing great information that helped us, we hope to do the same for others.

Hi Dan,

Did you end up joining Liberty in January? If so, how did I get?

Thank you!

Leslie

*

“how did it go” (wow, sorry! haha)

I liked your post and Thanks for sharing. My wife and I belong to Christian Healthcare Ministries and love it. It beats the sox off traditional plans out there, no pesky annoying insurance agent bugging you either!! The plan is very affordable and meets all the AHC act. guides.

Well, good for you, but would you care to compare Christian Healthcare to Liberty, so that we can all see the differences? Can you share some examples? Christian Healthcare supposedly only covers bills in excess of $5,000, as I understand it.

Liberty excludes activities like rock climbing, etc. I need to find a sharing group that does not exclude occasional fun outdoors activities and also doesn’t require a pastor to sign off on every single doctor visit.

I have been studying Liberty extensively, last year and this year (right now. My $200/high deductible plan in 2016 became a $500/high deductible plan in 2017, and finally $700/mth high deductible plan this year. Enough is enough!)

In any case…I haven’t been able to find anything that says Liberty excludes sharing for costs incurred due to medical events experienced in any specific type of activity. Please cite a source for your comment, otherwise don’t post incorrect information.

My apologies Carl…I missed it when I read through the downloaded guidelines the first time. As per those guidelines:

“Examples of hazardous hobbies include, but are not limited to, rock/cliff climbing, spelunking, skydiving, or bungee jumping.” What’s interesting, and is a huge example of the difference between sharing and actual insurance, is that and insurance contract states very specifically what is covered and what is not.. With Liberty Health Share, the items mentioned are not covered, but the real gotcha is “but are not limited to.” I’m a downhill skier. Covered? Hopefully. I hike in the desert. Covered? Hopefully. I ride a mountain bike. Covered? Hopefully.

This does provide another level of scrutiny, as some of my activities are not “not covered,” but also might not be…based on whose decision? It’s a mountain bike crash or a skiing accident that would likely cause me a visit to the hospital thus far. Hmmm. I could call and ask, but obviously nothing I am ‘told’ will have any authority down the line when it’s decided my injury was caused by a ‘hazardous’ hobby.

great comment.. I ski and thanks for highlighting this.

I signed on with Liberty Health Share. It’s been a huge disappointment. I have been sent to collection due to their lack of care with my case. I recieved a bill from the hospital where I had knee surgery. They paid just over $5,000.00 of an $18,000.00 bill. They told me that the hospital was trying to over charge and they would resolve it for me. They advised me not to pay anything until they had it settled. They had sent my information to AMMPS. they did nothing with the bill nor did it get resolved. I was advised to ignore the calls from people trying to collect. I numerous times notified them of every bill even faxed them directly to them. Finally one day when I called them they said that Ammps had dropped the ball on their accounts so the are now with MEDCost Solutions. Guess what, Nothing has been resolved I talked to them today was told that a superviser would call me and they would make this an urgent matter.Never recieved a call back now I’m sitting here with a huge bill and bad credit. I had Amazing credit before this. My advise to anyone who is thinking of using Liberty Health Share, do your home work and read all the reviews.

Hi Wendy – did this ever get resolved?

Hi Michelle – such a relevant and informative post! I was so unhappy with the cost of my insurance plan, so we made the switch January 1, 2018. We are set to save $18,000 this year because of the switch. I wrote about my experience choosing a Health Share ministry and did a little comparison to help others in this journey here: https://broketobeach.com/2018/01/21/health-share-ministry-versus-health-insurance/

Any updates to share about your experience? I’d love to hear them!

Cheers!