Liberty Healthshare Review Update June 8, 2022 – I personally used Liberty HealthShare for the birth of my daughter in late December of 2021. All of my medical bills were paid quickly and I am happy with the service that I received.

Liberty Healthshare Review Update May 20, 2024 – My husband had a minor surgery this year and it was paid for with no problems as well.

Okay, okay, hear me out first. I want to start out this Liberty HealthShare review and state that this is not a political post, at all. Seriously. This also isn’t a sponsored post or anything like that. This is my Liberty HealthShare review and my research on a health care sharing ministry, as I want to help others find alternative forms of health insurance in case they need it. I did. If you are looking for Liberty Healthshare reviews, then here is my opinion.

I first heard about health sharing ministries about a year ago. I had no idea that they existed, but I thought it was an interesting concept. I didn’t look into it any further because I already had health insurance.

Then, in late 2015, I found out that I had no realistic health insurance options. I didn’t want to pay the penalty for not having health insurance, and I also didn’t want to go uninsured.

See, for full-time RVers, health insurance companies are fairly strict.

Some health insurance companies won’t cover you once you travel away from your state. If they do cover you when out-of-state, they usually require that you at least live full-time in your home state. As RVers, while we do have an address, it is technically not where we live full-time, so we did not want to have to deal with a health insurance company possibly voiding a medical expense if they found out that we were trying to get around this loophole.

Plus, the only policy that we qualified for (in our state) had an astonishing deductible of $39,000 for an out-of-state medical expense. And, as full-time RVers, we are excluded from the majority of policies anyways due to the loophole as described above, so that just didn’t work for us.

Paying a high monthly health insurance premium that comes with a $39,000 annual deductible, and the fact that any of our claims would probably be voided because we are full-time travelers, made this decision a no-brainer.

We obviously had to find something else.

Related blog posts if you’re interested in this Liberty Healthshare Review:

- 30+ Ways To Save Thousands of Dollars a Month

- 75+ Ways To Make Extra Money

- How To Take A 10 Day Trip To Hawaii For $22.40

- The $20 Savings Challenge

So, in January of 2016, we started a membership with Liberty HealthShare. We filled out an application, they approved us, and we even had a medical expense in January that they covered. We NEVER have medical expenses, so it was just a coincidence that we had a claim only six days after we were approved.

And, they covered that claim.

My Liberty Healthshare review:

So, what is a health care sharing ministry?

According to Healthcaresharing.org, “a health care sharing ministry provides a health care cost sharing arrangement among persons of similar and sincerely held beliefs. HCSMs are operated by not-for-profit religious organizations acting as a clearinghouse for those who have medical expenses and those who desire to share the burden of those medical expenses.”

Members of a health sharing ministry pay a monthly share with an agreement to help one another in the risk-pool by covering medical expenses.

The positives of a health care sharing ministry.

The positives of health sharing ministries include:

- Monthly costs that can be much less expensive than traditional health insurance.

- Lower annual deductibles.

- No in-network requirements, so you can go to any doctor, hospital, etc., that you wish.

Also, being a member of Liberty HealthShare exempts you from paying the penalty for not having health insurance.

How much is Liberty HealthShare?

For the three of us, we pay $874 each month.

With this monthly share, “Up to $1,000,000 (per incident) of fair & reasonable eligible medical expenses are shareable after AUA has been met.”

They even have plans for as low as $89 per month.

You can find all of Liberty HealthShare’s options here.

The downsides of a health care sharing ministry.

Now, health sharing ministries are definitely not perfect. As with most things, something this good must have negatives.

Liberty HealthShare is not traditional health insurance, which means:

- They are under no requirement to cover your medical expenses.

- You cannot deduct Liberty’s monthly costs from your business taxes.

- You cannot contribute to a Health Savings Account.

- Pre-existing medical conditions are not covered until years later.

Health care sharing ministries all have some sort of ethical rules that you must abide by such as no smoking, no drinking, and so on. If you incur a medical expense due to something that is against their policies, there is a chance that they will not cover it.

Lastly, I want to repeat this again, the biggest caveat is that there is no guarantee that a health sharing ministry will pay a medical expense. This is because they are not governed under the same laws as health insurance companies due to the fact that they are not considered health insurance.

Related: Do you need travel medical insurance if you travel long-term?

Liberty HealthShare review

First of all, leaving traditional health insurance and joining a health sharing ministry was a difficult decision for us. We’ve always had “normal” health insurance, and we don’t know many people who use Liberty.

However, we didn’t really have a choice.

We even used an RV health insurance broker to see if they could find us anything, which they couldn’t. It was either be completely uninsured or go the health care sharing ministry route.

I will say that I haven’t regretted this decision one bit. So far, I have had no problems with Liberty HealthShare. They have covered one wellness visit as well as an ER visit. It was pretty easy in both cases- they just took my Liberty HealthShare card and didn’t have any questions. Liberty HealthShare didn’t have any questions either.

Liberty HealthShare does have a set of guidelines (which you can find here) that they ask that you follow. But, they accept customers of all faiths, lifestyles, backgrounds, and sexual orientations.

Here are links to Liberty Healthshare’s rules on other questions you may have:

- Liberty Healthshare pregnancy – Maternity & Membership: What to Expect

- Frequently Asked Questions

I will make sure to keep this Liberty HealthShare review updated in case anything happens, especially if my opinion were to change in the future.

How did I hear about this health care sharing ministry?

There were two main people who influenced my decision to join Liberty HealthShare. This includes Holly and Choncé. Both of them are Liberty HealthShare members, and here is what they have to say about the company:

We joined Liberty HealthShare in 2014 after seeing our premiums double due to the Affordable Care Act. So far, we have seen tremendous value with our plan, and all for a price that is half of what we would need to pay for health insurance. And, instead of having a $12,000 or $13,000 deductible with Obamacare, we have a $1,500 annual out-of-pocket max. – Holly Johnson at Club Thrifty, Why We’re Joining a Healthcare Sharing Ministry

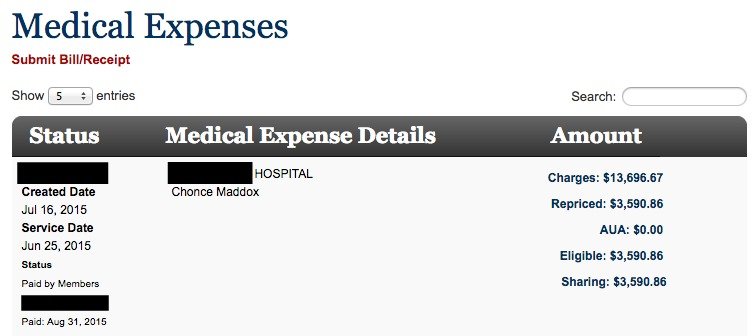

I’ve been using Liberty HealthShare for about a year and a half now. At first, I was hesitant to try it, but health insurance premium quotes were very high for me so I knew I didn’t have much to lose. Now, I am so happy I gave it a try because I like how I can visit any doctor I want and Liberty has really stepped up to share my medical expenses so I don’t have to cover them out of pocket. Last year, I had to have a surgery done which totaled around $13,600. Liberty HealthShare repriced my medical bills to about $3,500 and shared the entire expense. Having surgery is scary enough on its own, but I felt peace-of-mind knowing I wasn’t going to be bombarded with tons of unnecessary medical expenses afterward. Liberty HealthShare is still growing and the team is always open to hearing suggestions and trying to improve each member’s experience. I like how one team member offered to call a doctor I was interested in seeing to explain to them what a health sharing ministry is and ask if they would accept me as a patient. – Choncé at My Debt Epiphany, Putting My Health First: A Review of Liberty HealthShare

Choncé was also kind enough to share a screenshot of how Liberty HealthShare paid the entire expense of a surgery she had last year.

If you’re interested in Liberty HealthShare after reading my Liberty HealthShare review, please send me an email at michelle@makingsenseofcents.com, and I can put you in touch with someone at the company. They will explain it further and answer any questions you have..

How much do you pay monthly for health insurance or an alternative? What do you think of health care sharing ministries?

Disclaimer with this Liberty HealthShare review: You should always do your own research when it comes to a big topic such as choosing health care, a health care sharing ministry, and health insurance. This is just my opinion and review of Liberty HealthShare, but you should remember that I am not a health care professional or expert.

Leave a Reply

Wow. Just one more caveat to being an RV living family that I never even thought about. I do naturally wonder what self-employed folks are doing for health insurance, and how much, but the whole RV thing adds another layer. I’m glad you found something reasonable to comply with the law and get health care needs met. The part about them not being required to cover you sounds so crazy, but it sounds like you really had no other options.

Yes, there are lots of things to think about when it comes to RVing!

I was so excited to see your post. I had to put two of our children on this plan as our family moved to an HMO that wouldn’t cover them as they are out of the state. There are 4 sharing companies, I believe. When the ACA was being written someone was smart enough to get language inserted that if the company existed prior to some year (1995? or maybe 1985?), members (new or existing) of those would be exempt from the penalty of not having traditional insurance.

This month will be the first time we have tried to use it, so maybe I will come back and leave a review of our experience. I liked Liberty Health over the others because after 3-years, pre-existing conditions are covered, where as the other companies don’t cover them. Also, Liberty operates more traditionally in that they collect all of the “premiums” and distribute as necessary. Many of the other companies had you write individual checks to the other members.

We did opt for the higher plan which either has a much higher lifetime max or no max, I can’t remember and it comes with a bill negotiation feature.

I did a ton of research on these companies and it was very difficult to find any bad experiences. The reason we didn’t move over as a family is the company I work for contributes part of the costs and wouldn’t switch over to them. I also have an HSA eligible plan. Liberty Healthshare does not qualify for an HSA.

Great to hear from a fellow member! Liberty’s highest amount is $1,000,000, which is the plan that me and my husband are on.

Wow I had no idea that you had to have a special form of insurance if you move frequently from one state to another. Thank you for the content, I also had no idea this even existed. I see the downside to using this service and will be researching further. I just signed up for my employer’s health insurance benefits and hopefully that’s enough for now.

Health is so important!

I’m an early retiree and have been on Obamacare for 2 years (retired at 53). I’ve seen it go up in cost and down in value and choice tremendously. I’ve been researching alternatives for a while now and Liberty is on top of my list. You being a full-time RV’er bring up another consideration – full-time traveling. I spoke with Kim at Liberty and he assures me they will cover me internationally as well as domestically. I may need to pay the expense first and then be reimbursed but that should not be a problem unless it is $$$.

Do you or any of your readers have any experience with Liberty and international travel or living?

I’m really interested to know the answer to this too – I travel internationally quite a bit and I’m about to become a full-time RVer when I’m in the US. Thanks!

I am so glad you wrote this post! I had never thought about what traveling full time could mean for my health insurance coverage. Do you know if life insurance policies are similar in regard to full time travelers?

Thanks again because this was ridiculously informative!

Amanda

I haven’t really looked too far into life insurance policies since we started traveling. That’s something I definitely need to do!

Thanks for sharing. Health insurance has turned into golden handcuffs for us. It’s the one obstacle keeping us from living our dream. I had no idea these ministry plans were so affordable. The skeptic is me did a quick search “Christian health ministries – do they pay claims?” which turned up this article from the New York Times on the first page: http://www.nytimes.com/2015/02/01/opinion/sunday/onward-christian-health-care.html It starts with a story of a breast cancer patient and how her claims were addressed. It’s just one story though and that’s anecdotal. It’s still encouraging!!

Hi Michelle,

Thanks for posting.

This blog post comes handy. My health insurance is up for renewal, and I had to change some condition because like you, I’m going to travel/live in three different countries in yearly basis which make me a digital nomad.

The result is my insurance has triple the premium, which don’t make me very happy.

I just wrote an article about my decision process if accept the new premium or stay uninsured while investing this money by myself.

In effect, creating my own insurance. The idea is to use this portfolio for future medical bills expenses when needed.

I’m still analyzing and processing “alternative” ideas.

I’m going to check out the “health care sharing ministry.” It sounds interesting.

Hopefully, there is an international one. I’m not American.

Hi Michelle,

Thanks so much for posting this. Has it continued to work out for you guys? Some reviews said that it took over a year for the bills to be settled.

I’m also a bit concerned that it’s such a small company. I read somewhere that it only has < 30,000 people signed up, which isn't much to share the risk and a lot of these companies have gone out of business lately. It also caps the amount covered per incident, and cancer/surgery/chemo, treatment for hepatitis, or a bad car accident can easily blow through this cap. The likelihood of being in this scenario is low, but as a doc I do see it all the time. They also state that if you file too many claims, they'll raise your rates. So again, if you get cancer…

I also wish that they accepted pre-existing conditions, because by pulling healthy people out of the ACA pool, they raise the prices for everyone else.

Argh! I wish we had better options, and thanks again for the review.

Yes, it’s worked out for us and they have covered a few small bills already. That being said, there weren’t any other options for us since we’re RVers and normal insurance or ACA won’t cover us.

The Liberty group I’m a part of has a cap of $1,000,000 per incident. I figure that’s enough. If I have a medical situation that costs more than a million dollars, I got bigger problems than bankruptcy. And back to what the author points out a few times–I had not choice. OK, so I do have a choice, but the cost of traditional insurance is approaching unobtainable, and thus “no choice” but to do something alternative.

You do raise a good point that if a significant part of the population joins healthshares, it leaves a higher concentration of folks needing more expensive care in the insurance pools. Those needs have to be met SOMEHOW, and most likely the government has to step in and pay…which means we pay with higher taxes.

What needs to happen is to reduce the costs in the first place. In the US, we spend 2300% more on health care in 2009 than we did in 1970. The data shows that this is primarily due to increased administration costs! That is, the insurance industry and government regulation has complicated the system so much, we are now spending billions just to process our health care paperwork and billing. I highlight this in an article I wrote this week: https://www.linkedin.com/pulse/insurance-kills-healthcare-part-2-troy-wolf

I am getting mixed inputs on the # of members that are part of Liberty HealthSharing. When I call they say it has 70,000. But then other sites are claiming it has only20 or 30,000. Do you know how many members they have now?

I recently joined Liberty Direct–part of Liberty Healthshare. On Dec 22, 2016, I received an email from Liberty’s Executive Director, Dale Bellis, that said, “Just a few days ago, our membership surpassed 100,000 people!”

I wonder how is it possible that Liberty Health Share can convince any hospital or healthcare provider to reduce their costs upwards of 75% to 85% ? I read a few examples where a member would have a major healthcare event and Liberty would simply convince the hospital to re-price their bill. One example was for a cancer treatment in the amount of $380,000. Liberty somehow convinced the hospital to re-price it down to less than $80,000. I have some experience in this field and I know that most hospitals will not consider cost reductions under any circumstances. I am very surprised to read this and quite frankly, it now makes me wonder what happens if the hospital or healthcare provider says “no”. Does Liberty still go through with the reimbursement or simply pay what they think it should cost no matter if the real cost is much higher ???

They say they will pay the whole amount that is due, whether it can be reduced or not.

Great article. It’s great to have multiple options so you can make the best decision for your family. That being said, there are other options for those that want actual insurance outside of Obamacare. My family and I are on a plan that saved us over 70% from Obamacare/ACA and it’s a nationwide plan so I can get coverage whenever my family and I travel in the USA.

Do you mind sharing what your plan is?

Did TR ever share plan information?

I’m also curious as to what plan your family is on. Do you mind sharing? Thank you!!

Wow, that 39k deductible for traditional insurance that you were quoted on is bonkers! I can’t get over their greed.

Glad to hear you found a good alternative and hope it continues to work out well!

This article is better than mine, but I just published an article on LinkedIn about my healthcare journey that includes a health care sharing ministry. https://www.linkedin.com/pulse/insurance-kills-healthcare-part-2-troy-wolf

Thanks for sharing your experience and spreading the word!

I just recently got a quote for my family (of four) after discussing my preexisting condition- leukemia. I was told while my condition was not going to be shared, my other health care concerns would be if they arose. My leukemia is in a “progression free survival” mode managed with Imbruvica at 20k / month. With private pay insurance Johnson & Johnson will provide the drug free at my income level but not with “single payer- (read public)”. After submitting the application, I was informed that I would not be covered for any care for any condition even if unrelated to my preexisting condition. The website informs the public that no coverage for the preexisting condition DURING the first year of coverage, 25,000 for the 2nd year and 50,000 for the third year.

I think they should change this to be consistent with actual practice of not sharing at all ANYONE with a preexisting condition.

My husband and I are both self employed. We always paid for our own health insurance for the two of us and our two children. Since The Affordable Care Act was put in place our premiums have been unsustainable and we were forced to go through the exchange to keep costs down, but those premiums became unsustainable as well. Insurance premiums should not equal a mortgage payment! In my search for an alternative I stumbled upon Liberty HealthShare and took a chance. I just signed on this January 2017. I am so relieved to read this article. We haven’t had any medical expenses yet, but I’m relieved to know they cover them! More than I can say for the regular health insurance companies who find every reason possible to deny a claim. Thanks for the info!

I’m about to take the leap too–best of luck to you; I hope you post your experience. I will as well.

Since I’m health, and fit, I don’t anticipate NEEDING more than my annual check ups, but of course you just never know.

Thanks for sharing this information. My hubby and I are exploring our health insurance options as we look to early retirement. We have a blog that we are building and hope to build it to a level where we can travel nearly full-time in our Airstream. I appreciate all the assistance and advice that I get from your blog!

RV living is so much fun! 🙂